Content Distribution Faces New Challenges, Opportunities

Content Insider – NAB Ads

By Andy Marken – andy@markencom.com

“Advertising is based on one thing: happiness. You know what happiness is? Happiness is smell of a new car. It’s freedom from fear. It’s a billboard on the side of the road that screams with reassurance that whatever you’re doing, it’s okay. You are okay.” – Dan Draper, “Mad Men,” Lionsgate, 2007-2015

Vegas was rockin’ and buzzin’ last week as the town hosted a refreshed NAB and squeezed in the happier than h*** CinemaCon.

The big chatter at both shows was Netflix’s surprising drop in subscribers, reaffirming to attendees that folks can only tolerate/afford so much ad-free paid content; and obviously, the steadily dwindling movie house numbers are still a solid bet for studios and consumers.

Over at CinemaCon, Sony’s film chief Tom Rothman couldn’t contain himself, “Netflix, my ass.”

True, he’s just one of five studios that doesn’t have its own streaming service, hasn’t sold a lot of content to the subscription streamer and really needs to get as much support and cash from theater owners – and their audiences – before he negotiates with streaming services and/or Pay TV folks.

The big boys – Disney, Warner, Paramount, MGM (now part of Amazon), Universal (part of Comcast/Peacock) – have their feet in both camps and give theatrical windows ranging from 17 – 45 days before the projects appear on their services.

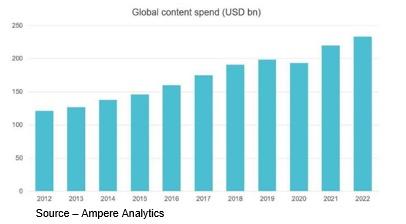

Content Spend – Today, video storytellers have a wide array of sales opportunities – movie houses, Pay TV, streaming: AVOD/SVOD – and they all need to keep their pipelines filled to attract an audience. Where do normal folks spend most of their viewing time? At home. Source – Ampere Analytics

Rothman also sidestepped the fact that a third of the projects of the content creation industry went directly to streamers.

Investments – Thanks to the build-out of streaming services and the need for content for entertainment around the globe; studios, streamers and others will invest $230B in fresh movies/series.

More importantly for the folks who produce video stories, the industry – theatrical, Pay TV, streaming – will be investing an estimated $230B this year to make stuff for people to watch.

Studios spaces are also feeling the pinch with new production space being built across Canada, Africa, the Middle East and Europe, including more than 6M sq ft planned/under construction in the UK.

Much of the content will never be shown in their houses because theatrical folks count on the big budget tentpoles to attract people to put seats in seats while they gloss over the fact that:

- Theater attendance has fallen steadily since 2002

- Theaters make up the difference by steadily raising ticket/concession prices

- Studios foot all of the marketing costs to attract the audience

- 70 percent of the audience will prefer to watch a movie at home (Variety)

At the same time, that level of investment can’t be maintained solely by subscription services.

Big Questions

The show floor and sessions were abuzz at NAB with key questions and a ton of educated/uneducated speculation:

- Does the first drop in 10 years forecast the streaming giant is falling back to earth?

- How many ads are best in the streamers?

- How much data will streamers use/share to make ads inviting/effective?

- How will consumers balance their desire/budget?

- What’s next?

Listen to Them

While WarnerBros Discovery’s CFO Gunnar Wiedenfels was focusing on his own company’s issues of mashing/slashing everything together, he prophetically summarized the challenges/opportunities facing the entire M&E industry (theatrical, Pay TV and streaming) when he said, “2022 [would] undoubtedly be a messy year.”

And probably through 2024.

Discounting the 700K Russian subscribers Netflix dropped, the company – still with more than 200M subscribers worldwide, proved there is a limit as to how much consumers will pay before they say, “enough is enough.”

Folks told Netflix’s Hastings – and the rest – that some level of advertising is okay in return for a reasonable any time, any place, any screen streaming entertainment.

All of the services, including Netflix, base their subscription prices to a greater or lesser degree on the economies of the individual countries and consumer income/budget indexes.

European subscribers had already pushed back moving to ad-subsidized services while they have been preferred since the beginning by families in Asia.

According to Statista:

- Streaming user penetration – SVOD, AVOD – in the Americas is 40 percent and expected to hit 43.3 percent by 2026 or 224.6M users

- Globally user penetration is 25.5 percent this year and projected to hit 29.2 percent by 2026 or 2.3B users

Netflix will face a tough couple of years as it determines the best approach/balance for paid, subsidized and free streaming while making continued investments in new, unique content regionally and globally.

Growth – There are more than 2.5B TV-enabled households around the world and the streaming services have only attracted the easy picking folks. Now they need to continue to grow with an array of opportunities, entertainment, pricing.

So does everyone else – those with global aspirations (Disney including Hulu, WarnerBros including HBO, Amazon, Tencent, iQiyi, YouTube, Paramount, Apple) as well as regional players (Comcast/Peacock, ALTBalaji, Rakuten, Viaplay, Zee5, Shahid, BritBox and 200+ others).

For the next few years there will be blood on the sand!

Constructing Tiers

Budget Balancing – Consumers have quickly found that they can reach their peak entertainment budget by going totally SVOD and today want options.

Because of its firm stance on ad-free content, figuring out the ad thing is one of the few areas Netflix doesn’t lead.

Hulu has had tiered pricing since the beginning and as soon as Disney (which already includes India’s Hotstar) rolls it into their service (they only own 60 percent … now) we’ll see three-tier pricing – no ads, some ads, more ads.

As soon as WarnerBros Discovery’s Zaslav has cleaned up the merger mess, he and his team will focus on their tiered offerings. HBO has gone through a number of tier macerations so bringing the “new” company under a single umbrella with easy-to-understand consumer cost options shouldn’t be too difficult. The toughest part might be what to call it!

China’s Tencent and iQiyi are creeping across Asia/Southeast Asia and may only have regional aspirations, but it’s a big market of about 3B of the nearly 8B people on the planet. With China’s economy in disarray, we’re certain the government won’t subsidize their growth so tiers/profits will be important.

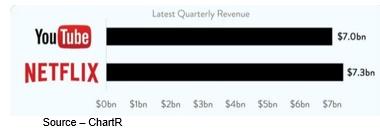

Big Dogs – Much as most of the M&E folks like to discount the entertainment value of YouTube, it is still the most widely used online video channel around the globe.

Folks at NAB said, “who cares about YouTube they’re just a place for kid and marketing videos,” but we’re pretty certain YouTube CEO Susan Wojcicki has big entertainment plans for the service that has 2.2B users and 50M premium users.

Getting the GenZers involved with them early makes it easier to keep them “in the habit” as they become the millennials of tomorrow.

Never take a smart female for granted!

ViacomCBS’s Paramount is long on aspirations and just beginning to expand its content base, pricing structure and subscriptions with 56M global subscribers.

Viacom’s Sheri Sumner and ViacomCBS’s CEO Bob Bakish are moving cautiously from the bottom up with free viewing first and moving up the tiers from there.

And then there’s Comcast/NBCUniversal’s Peacock.

Little Tired – Comcast’s NBCUniversal Peacock has had a tough time learning how to fly in the D2C arena, but there is a chance it will get its second wind and take to the air.

When Comcast acquired Britain’s Sky, they became one of the planet’s cable connections to the home and pay TV giants. Both areas are highly profitable and still relatively strong/stable. Owning the last 100 feet to the home is predictable and profitable.

Pay TV is staying steady – 1.5B globally – and growing slightly – .5 percent everywhere except in the US. More importantly, for the established players, no new folks are jumping into “their” market.

Peacock is just another channel ViacomCBSUniversal can use to monetize its content.

People have long told entertainment providers they’ll swap a little bit of their time to get their content free or at a nice discount.

Time is Money – While all of the studios and networks headed for the same door as Netflix to snap up and grow their streaming subscribers, consumers have said loud and clear that if you treat us right, we’re happy to trade some eyeball time for your content and a few ads.

It shouldn’t have come as a big surprise to anyone that people didn’t really mind ads.

In fact, they can be a nice break from the excitement/horror of the show they’re watching.

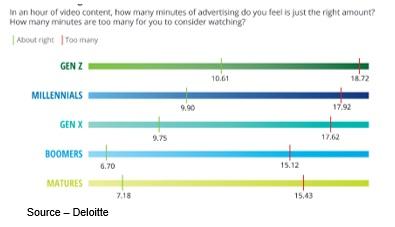

They just don’t want 20 minutes of ads packed into their hour of entertainment.

Just Right – The biggest challenge for streaming services (all of them) is trying to figure out how many ads people will tolerate. Certainly, 20 minutes of ads per hour isn’t it because that’s one of the reasons they cut the bundle cord.

The key for streaming services is to develop tiers of service so subscribers know how many minutes of time she/he is “paying” for the entertainment.

For example, no ads for a premium plus subscription, 2-3 minutes an hour for a premium plan, 10 minutes of ads in an hour for free viewing.

Anything over 10ish minutes and there was no reason to spend days/months fighting with your pay TV bundle provider to escape their grasp.

The key for Hastings and his CFO (have you noticed you haven’t heard from his co-CEO– just saying) as well as all of the other streamers is to figure out what the right balance for each tier is right for the consumer and right for their bottom line.

Content is expensive and perishable, so you have to determine how much money you’re going to need to keep the streaming pipeline filled with new stuff and pay for other things like shareholder dividends and executive salaries.

Streaming services already offer lighter ad loads — 4 to 8 minutes per hour, compared to 17 minutes on day/time TV. While consumers have said they would like even fewer ads (financially impractical) there is a way to make ads palatable.

Services need to get rid of the old-fashioned commercial block and try options like pre or mid movie/show mini ads grouping.

Rather than buy/sell ads in the old way your father did (1000s of households), streaming allows services and marketers to selectively deliver specific audience segments/categories based on comprehensive user information.

That makes the subscribers more interesting/more valuable.

Imagine the thrill of seeing ads that offer information on interesting places to visit because you’re planning a holiday, underwear because yours have holes or car info because you’re considering a new vehicle rather than 15 ads from ambulance-chasing lawyers.

To bother viewers less, streaming services are starting to move away from the traditional block of commercials and experiment with ad breaks, interactive ad formats and other new models enabled by the internet.

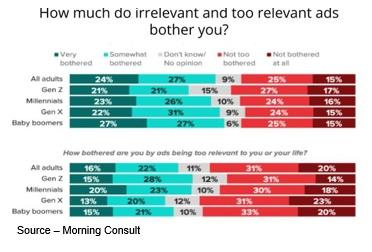

Gentle Touch – People don’t like a ton of stupid ads, but they also don’t want too many ads that are really pertinent to them … that’s creepy. Relevance is going to be tricky in the new environment.

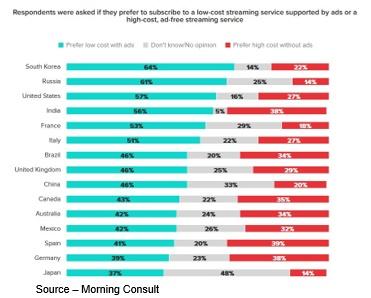

Nearly 60 percent the people surveyed by Morning Consult indicated targeted ads are informative. Half indicated they were helpful.

Now that streamers have developed a greater database of viewers’ information to help them greenlight content, folks want to see ads that can be more targeted – but not too targeted – and personalized – but not too personalized.

There’s a balance the streamer and advertiser have to strike that enables them to reach the right audience with the right message while respecting their privacy.

There’s a fine line between being valuable and of assistance and being creepy.

Advertisers have been eager to get into business with Netflix for years.

Catch the Wave – When everything is just right, everyone wants to catch the wave and have a successful (profitable) ride; but sometimes, some of the waveriders will have a wipeout because the place is too crowded.

There’s a big difference between their nearly 222M worldwide subscribers and 74.6M in the Americas compared to Disney’s 196M globally and 42.9M in the Americas; or WarnerBros Discovery/HBO’s 100M global, 55M Americas.

In addition, they have a rich subscriber database … and know how to use it.

Rich subscriber data and lighter ad loads should enable them to charge more for ads as long as they can manage the expectations of subscribers and marketers.

Publicly available viewer data for streaming programming from any/all of the entertainment monitoring services remains slim.

Disney, Warner Bros. Discovery, NBCUniversal Paramount Global and all the rest have a long relationship with advertising but are extremely shy about divulging any viewer data.

The two streamers not included in this discussion are Amazon Prime and Apple TV+ because they have taken different paths.

Lord of the Rings – Amazon has a “slightly different” model for their subscription video service including a newly renamed free service – IMDb TV to Freevee??? – so all services aren’t created equal.

Amazon has probably reached its price ceiling, having raised its annual membership to $139, which helps when they’re spending about $500M on the first chapter of Lord of the Rings and signed on Thursday Night Football.

The addition of MGM’s content helped the company record more than 175M Amazon Prime members. And to attract the free, ad-supported viewers, they renamed IMDb TV to Freevee (really?) and have committed to expanding the programming budget for the service.

Gentle Giant – The move into the streaming video marketplace was inevitable for Apple because it already had a strong relationship with content creators and most important, with screen users. Now they may be ready for the next move.

With an Oscar sitting on it’s shelf for CODA, Apple TV+ clearly made its mark in the content creation/streaming arena, despite a relatively quiet launch.

They also know how to run with what works – ordering two more seasons of Ted Lasso, reboots of Saved by the Bell, Punky Brewster, Gossip Girl and more old series are being planned or released.

But with more than 1.8B device users worldwide, the company also has an active installed base of iPhone, iPad, Mac, Apple Watch and Apple TV units. In addition, it has loyal – almost devoted – users of their music, healthcare, games, written materials and in all, more than 1.8M applications worldwide.

Apps that 825M people pay to use.

And, it’s all in a walled garden that prides itself on privacy, security and content.

The most interesting/intriguing rumor is that they may begin a “don’t buy it, lease it” program which could dramatically boost hardware in users’ hands/homes and include levels of content consumption.

Damn!

Suddenly, they could be a competitor and potential partner with every other streaming service, everywhere.

Still, that’s only a rumor.

But there were more questions than answers regarding what the next generation of subscription and ad-driven entertainment will look like.

Streaming service opportunities are definitely on the short list for content producers, services and advertisers.

Everyone – including consumers – is interested in expanding their reach beyond appointment TV as they explore new ways of monetizing content.

Streaming intelligent, informative, interesting commercials will be an exciting learning experience for everyone, including consumers who can’t continue paying for five or more subscription services.

Source – “Mad Men,” Lionsgate

But we think the industry is up to the challenge.

As Don Draper said in Mad Men, “Send him in.”

We’ll find out more about how folks have progressed at IBC and NAB next year.

Andy Marken – andy@markencom.com – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.