Spotify Technology S.A. Announces Financial Results for Second Quarter 2021

NEW YORK–(BUSINESS WIRE)–Spotify Technology S.A. (NYSE:SPOT):

![]()

Dear Shareholders,

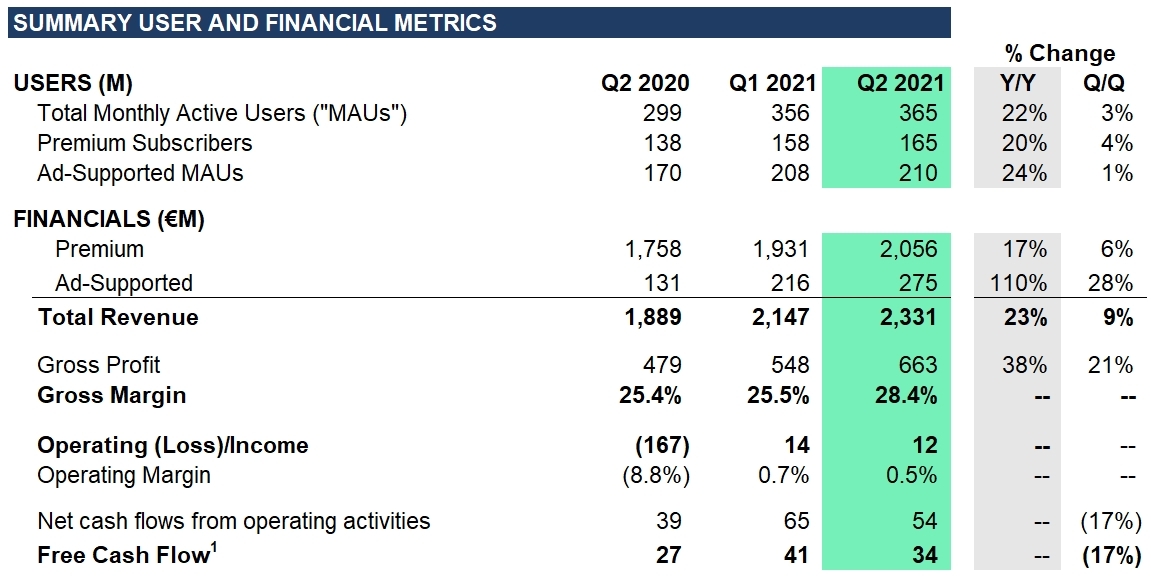

Most of our major metrics — Subscriber growth, Revenue, Gross Margin, and Operating Income — performed better than expected this quarter. The exception was MAUs, where we fell short of our guidance range. The quarter was led by improving ARPU, decreased churn, a return to per user consumption growth, and significant advertising strength. We did see a second quarter of greater MAU variability mainly due to ongoing COVID-19 headwinds and a temporary issue related to user intake on a third party platform. However, trends improved in the back half of the quarter. Additionally, we generated positive Free Cash Flow of €34 million.

MONTHLY ACTIVE USERS (“MAUs”)

Total MAUs grew 22% Y/Y to 365 million in the quarter, finishing below our guidance range and forecast. Despite our underperformance, we added 9 million MAUs in Q2, which drove double digit Y/Y growth in all regions.

MAU performance was slower than expected due primarily to lighter user intake during the first half of the quarter. COVID-19 continued to weigh on our performance in several markets, and, in some instances, we paused marketing campaigns due to the severity of the pandemic. Separately, a user sign-up issue associated with a global third party platform created unexpected intake friction, which also impacted MAU growth. This issue has since been resolved.

Overall, we saw a return to better growth patterns in the back half of the quarter. Although we continue to face near-term uncertainty with respect to COVID-19, we remain confident in the underlying health of our user funnel, and our existing user retention activity remains consistent with historical trends.

Global consumption hours continued to grow meaningfully in Q2 on a Y/Y basis. On a per user basis, global consumption levels returned to Y/Y growth in the quarter, led by gains in developed regions such as North America and Europe.

PREMIUM SUBSCRIBERS

Our Premium Subscribers grew 20% Y/Y to 165 million in the quarter, towards the upper end of our guidance range and modestly ahead of forecast. We added 7 million subscribers in Q2, which drove healthy double digit Y/Y growth across all regions. We saw strong performance of our Standard product across both Europe and North America.

Compared with the last few years, we shortened our mid-year promotional campaign cycle from 6 weeks to 4 weeks, and performance exceeded expectations. Additionally, we added or expanded several major promotional partnerships in the quarter, including a renewal and expansion of our Samsung promotion (offering 3 month trials in 73 markets to all new and existing mobile/speaker/wearable and appliance devices), a renewal and expansion of our Microsoft Gamepass promotion (offering 3 or 4 month trials in 15 markets), a new Epic/Fortnite promotion (3 month trial in 25 markets), a renewal of our Paypal promotion (3 month trial in 10 markets), and a renewal and expansion of our Vivo promotion (3 month trial in Brazil). Additionally, we announced a new promotion with TikTok (3 or 4 month trial across 7 countries in EMEA) which launched in mid July.

Our average monthly Premium churn rate for the quarter was down 23 bps Y/Y and down modestly Q/Q. The Y/Y improvement continues to be driven by the adoption of our higher retention offerings like Duo and Family Plans in addition to growth in high retention regions.

FINANCIAL METRICS

Revenue

Revenue of €2,331 million grew 23% Y/Y in Q2 (or 28% Y/Y on a constant currency basis) and was toward the top end of our guidance range due to significant advertising strength and subscriber outperformance. FX headwinds of 430 bps were 230 bps greater than expected, primarily driven by US dollar weakness vs. the Euro. Premium Revenue grew 17% Y/Y to €2,056 million (or 20% Y/Y constant currency) while Ad-Supported Revenue was particularly strong, growing 110% Y/Y to €275 million (or 126% Y/Y constant currency).

Within Premium, average revenue per user (“ARPU”) of €4.29 in Q2 was down 3% Y/Y (or flat Y/Y constant currency vs. down 1% Y/Y in Q1). Excluding the impact of FX, we saw a benefit to ARPU from our Q1 price increases along with a marginal initial impact from Q2 price increases, offset by the impact of product mix shift.

Ad-Supported Revenue outperformed our forecast, driven by strong underlying demand (benefiting sellout and pricing) and aided by favorable comps vs. last year’s COVID-19 lows. The strength in Ad-Supported Revenue was led by our Direct and Podcast sales channels, with the latter benefiting from a triple-digit Y/Y gain at existing Spotify studios (The Ringer, Parcast, Spotify Studios, and Gimlet) along with contributions from the Megaphone acquisition, the exclusive licensing of the Joe Rogan Experience, and Higher Ground. Ad Studio grew 165% Y/Y due to the success of the video product within Ad Studio and international market contributions.

We are very pleased with the initial performance of the Spotify Audience Network which launched in the US in April. The rollout allowed us to increase our monetizable podcast inventory in the US by nearly 3x. Additionally, for opted-in podcast publishers we’ve seen a double digit increase in fill rates, a meaningful increase in unique advertisers, and a double digit lift in CPMs. On July 1, we expanded the Spotify Audience Network to include Australia, Canada, and the United Kingdom.

Gross Margin

Gross Margin finished at 28.4% in Q2, above the top end of our guidance range and reflecting 308 bps of Y/Y expansion. While we did benefit from the release of accruals for prior period publishing royalty estimates, excluding the impact of these items, Gross Margin would have been 26.5%, ahead of our expectations. The Gross Margin improvement excluding these releases was driven by a favorable revenue mix shift towards podcasts, marketplace activity, and Other Cost of Revenue efficiencies (e.g. payment fees, streaming delivery costs), which were partially offset by higher non-music and other content costs and publishing rate increases.

Premium Gross Margin was 30.8% in Q2, up 261 bps Y/Y and Ad-Supported Gross Margin was 11.3% in Q2, up 2,321 bps Y/Y. As a reminder, all content costs related to podcast investment are included in the Ad-Supported business for the current and historical periods.

Operating Expenses

Operating Expenses totaled €651 million in Q2, an increase of 1% Y/Y (or 5% Y/Y constant currency) and in line with our plan. Excluding the benefits of currency movements, Operating Expenses were modestly higher than forecast as lower than expected marketing expenses arising from campaign timing shifts were offset by higher personnel costs.

Social Charges were approximately €2 million higher than forecast due to an increase in our share price during the quarter. Excluding the impact of Social Charges in both periods, Operating Expenses grew roughly in line with revenue. As a reminder, Social Charges are payroll taxes associated with employee salaries and benefits, including share-based compensation. We are subject to social taxes in several countries in which we operate, although Sweden accounts for the bulk of the social costs. We don’t forecast stock price changes in our guidance so upward or downward movements will impact our reported operating expenses.

At the end of Q2, our workforce consisted of 7,085 FTEs globally.

Product and Platform

During the quarter, we continued to increase the pace of our innovation efforts. On June 16, we soft-launched Spotify Greenroom, a redesigned version of Betty Lab’s Locker Room app, as part of our entry into the live audio space. This mobile app allows users to join or host live audio rooms, and optionally turn those conversations into podcasts. Additionally, we announced a Creator Fund bringing new exciting content to users and helping those creators get rewarded for the content they create on the platform. We expect to move to a full commercial launch of Spotify Greenroom later this year, with an initial focus on sports, pop culture, music, and entertainment.

During the quarter, we began rolling out our paid subscription platform for podcasters in the US. Additionally, as part of our Spotify Open Access platform strategy, we announced several new partnerships aimed at opening our platform to third-party paywalled content with the goal of becoming the world’s leading audio browser. On May 20, we partnered with Storytel, one of the world’s leading audiobook streaming services, to give Storytel subscribers the ability to enjoy their library of audiobooks on Spotify. On July 27, we announced more than 10 new Spotify Open Access partners — with more to come — all of which will be able to activate their subscriber base on Spotify while retaining full control over their content.

We continue to improve our search capability expanding our functionality to include filters and voice search making it quicker and more efficient for users to find content. Additionally, we rolled out a new version of Your Library to all Spotify mobile users that creates a streamlined way for listeners to explore their collection and find saved music and podcasts more easily.

During the quarter, we also advanced our product ubiquity efforts in a number of key areas. We introduced a new miniplayer experience that allows listeners to share, explore, and discover audio from Spotify directly within Facebook, without switching between apps. On the Apple Watch, we rolled out the capability for users to download playlists, albums, and podcasts to their watch. Finally, we expanded our video podcast footprint to Xbox gaming consoles and went live with the Spotify X1 integration to Rogers Communications customers in Canada.

Content

At the end of Q2, we had 2.9 million podcasts on the platform (up from 2.6 million at the end of Q1). The percentage of MAUs that engaged with podcast content on our platform improved modestly relative to Q1. Among MAUs that engaged with podcasts in Q2, consumption trends were strong (up 95% Y/Y in aggregate and more than 30% Y/Y on a per user basis) while week-over-week and month-over-month retention rates reached all-time highs. During the quarter, podcast share of overall consumption hours on our platform also reached an all-time high.

During the quarter, we announced exclusive licensing deals with Call Her Daddy and Armchair Expert, both of which are now exclusively on Spotify. The Joe Rogan Experience continues to perform above expectations, and The Ringer shows, such as The Bill Simmons Podcast, grew consumption significantly as the NBA headed into the playoffs.

Internationally, we released 100 new Originals & Exclusives (“O&E”) podcasts across markets including 5 adaptations of existing formats. We expanded Your Daily Drive to include Mexico (Ruta Diaria), Argentina (Ruta Diaria), and Brazil (Caminho Diário). The launches included bespoke content from 28 partners across the region, such as notable new organizations like Infobae and La Nación (Argentina), W Radio (Mexico), and 123 Segundos (Brazil), a Spotify original. One of the top podcasts in India, The Ranveer Show, which covers topics like health, spirituality, and lifestyle, also came exclusively to Spotify in June.

In Q2, Olivia Rodrigo’s album, SOUR, set the record for biggest streaming debut for any album on Spotify this year with over 63 million global first day streams. Other major releases in the quarter include BTS single, Butter, Griff’s Album, One Foot In Front Of The Other, and Doja Cat’s album, Planet Her. Spotify also launched a new Fresh Finds marketing program to celebrate Indie artists in the US as well as expanding the playlist via localized editions in 13 territories around the world. Fresh Finds, which first launched in 2016, has playlisted over 25,000 artists and built a reputation among users and in the industry as the go-to destination to discover new Indie acts. In addition, of artists whose first editorial playlist is Fresh Finds, over 44% go on to be playlisted in another editorial property on Spotify.

Two-Sided Marketplace

We continue to test Discovery Mode with a small set of labels and licensors including major labels, independent labels, and independent artist distributors. Thus far, artists with tracks in Discovery Mode have found over 40% more listeners on average compared to pre-Discovery Mode. Additionally, 44% of those listeners had never listened to the artist before. We are integrating feedback from our early partners with a broader rollout of Discovery Mode expected later this year with the main goal of facilitating more artist to fan connections.

Sponsored Recommendations (i.e. Marquee) continued to gain traction during the second quarter as we expanded into more international markets including Australia, Ireland, New Zealand, and the UK. We also rolled out new functionality for artist teams using the self-serve platform to target specific audience segments (casual listeners, lapsed listeners, and recently interested listeners) with their campaigns, a functionality previously only available to customers purchasing through our sales team.

Free Cash Flow

Free Cash Flow was €34 million in Q2, a €7 million increase Y/Y primarily due to an increase in net income adjusted for non-cash items, partially offset by higher working capital needs arising from select licensor payments (delayed from Q1), podcast-related payments, and higher ad-receivables. Capital expenditures increased €6 million Y/Y largely due to office build outs in LA, Berlin, and Miami.

At the end of Q2, we maintained a strong liquidity position with €3.1 billion in cash and cash equivalents, restricted cash, and short term investments.

Q3 & Q4 2021 OUTLOOK

The following forward-looking statements reflect Spotify’s expectations as of July 28, 2021 and are subject to substantial uncertainty. The estimates below utilize the same methodology we’ve used in prior quarters with respect to our guidance and the potential range of outcomes. Given the extraordinary operating circumstances we currently face with respect to the impact of COVID-19, there is a greater likelihood of variances with respect to those ranges than typical quarters.

Q3 2021 Guidance:

- Total MAUs: 377-382 million

- Total Premium Subscribers: 170-174 million

-

Total Revenue: €2.31-€2.51 billion

- Assumes approximately 60 bps tailwind to growth Y/Y due to movements in foreign exchange rates

- Gross Margin: 24.4-26.4%

- Operating Profit/Loss: €(80)-€0 million

Q4 2021 Guidance:

- Total MAUs: 400-407 million

- Total Premium Subscribers: 177-181 million

-

Total Revenue: €2.48-€2.68 billion

- Assumes approximately 175 bps tailwind to growth Y/Y due to movements in foreign exchange rates

- Gross Margin: 24.1-26.1%

- Operating Profit/Loss: €(152)-€(72) million

EARNINGS QUESTION & ANSWER SESSION

We will host a live question and answer session starting at 8 a.m. ET today on investors.spotify.com. Daniel Ek, our Founder and CEO, and Paul Vogel, our Chief Financial Officer, will be on hand to answer questions submitted through slido.com using the event code #SpotifyEarningsQ221. Participants also may join using the listen-only conference line by registering through the following site:

Direct Event Registration Portal: http://www.directeventreg.com/registration/event/6039475

We use investors.spotify.com and newsroom.spotify.com websites as well as other social media listed in the “Resources – Social Media” tab of our Investors website to disclose material company information.

Use of Non-IFRS Measures

To supplement our financial information presented in accordance with IFRS, we use the following non-IFRS financial measures: Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect, Ad-Supported revenue excluding foreign exchange effect, Gross margin excluding release of accruals for prior period publishing royalty estimate, Operating expense excluding foreign exchange effect, Operating expense excluding social charge, and Free Cash Flow. Management believes that Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect, Gross margin excluding release of accruals for prior period publishing royalty estimate, Operating expense excluding foreign exchange effect, Operating expense excluding social charge are useful to investors because they present measures that facilitate comparison to our historical performance. However, Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect, Ad-Supported revenue excluding foreign exchange effect, Gross margin excluding release of accruals for prior period publishing royalty estimate, Operating expense excluding foreign exchange effect, Operating expense excluding social charge, should be considered in addition to, not as a substitute for or superior to, Revenue, Premium revenue, Ad-Supported revenue, Gross margin, Operating expense or other financial measures prepared in accordance with IFRS. Management believes that Free Cash Flow is useful to investors because it presents a measure that approximates the amount of cash generated that is available to repay debt obligations, to make investments, and for certain other activities that exclude certain infrequently occurring and/or non-cash items. However, Free Cash Flow should be considered in addition to, not as a substitute for or superior to, net cash flows (used in)/from operating activities or other financial measures prepared in accordance with IFRS. For more information on these non-IFRS financial measures, please see “Reconciliation of IFRS to Non-IFRS Results” table.

Forward Looking Statements

This shareholder letter contains estimates and forward-looking statements. All statements other than statements of historical fact are forward-looking statements. The words “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible,” and similar words are intended to identify estimates and forward-looking statements.

Our estimates and forward-looking statements are mainly based on our current expectations and estimates of future events and trends, which affect or may affect our businesses and operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to numerous risks and uncertainties and are made in light of information currently available to us. Many important factors may adversely affect our results as indicated in forward-looking statements. These factors include, but are not limited to: our ability to attract prospective users and to retain existing users; competition for users, user listening time, and advertisers; risks associated with our international expansion and our ability to manage our growth; our ability to predict, recommend, and play content that our users enjoy; our ability to effectively monetize our Service; our ability to generate sufficient revenue to be profitable or to generate positive cash flow and grow on a sustained basis; risks associated with the expansion of our operations to deliver non-music content, including podcasts, including increased business, legal, financial, reputational, and competitive risks; potential disputes or liabilities associated with content made available on our Service; risks relating to the acquisition, investment, and disposition of companies or technologies; our dependence upon third-party licenses for most of the content we stream; our lack of control over the providers of our content and their effect on our access to music and other content; our ability to comply with the many complex license agreements to which we are a party; our ability to accurately estimate the amounts payable under our license agreements; the limitations on our operating flexibility due to the minimum guarantees required under certain of our license agreements; our ability to obtain accurate and comprehensive information about the compositions embodied in sound recordings in order to obtain necessary licenses or perform obligations under our existing license agreements; new copyright legislation and related regulations that may increase the cost and/or difficulty of music licensing; assertions by third parties of infringement or other violations by us of their intellectual property rights; our ability to protect our intellectual property; the dependence of streaming on operating systems, online platforms, hardware, networks, regulations, and standards that we do not control; potential breaches of our security systems or systems of third parties, including as a result of our Work From Anywhere program; interruptions, delays, or discontinuations in service in our systems or systems of third parties; changes in laws or regulations affecting us; risks relating to privacy and protection of user data; our ability to maintain, protect, and enhance our brand; payment-related risks; our ability to hire and retain key personnel, and challenges to productivity and integration as a result of our Work From Anywhere program; our ability to accurately estimate our user metrics and other estimates; risks associated with manipulation of stream counts and user accounts and unauthorized access to our services; tax-related risks; the concentration of voting power among our founders who have and will continue to have substantial control over our business; risks related to our status as a foreign private issuer; international, national or local economic, social or political conditions; risks associated with accounting estimates, currency fluctuations and foreign exchange controls; and the impact of the COVID-19 pandemic on our business and operations, including any adverse impact on advertising sales or subscriber revenue; risks related to our debt, including limitations on our cash flow for operations and our ability to satisfy our obligations under the Exchangeable Notes; our ability to raise the funds necessary to repurchase the Exchangeable Notes for cash, under certain circumstances, or to pay any cash amounts due upon exchange; provisions in the indenture governing the Exchangeable Notes delaying or preventing an otherwise beneficial takeover of us; and any adverse impact on our reported financial condition and results from the accounting methods for the Exchangeable Notes. A detailed discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from our estimates and forward-looking statements is included in our filings with the U.S. Securities and Exchange Commission (“SEC”), including our Annual Report on Form 20-F filed with the SEC on February 5, 2021, as updated by subsequently filed reports for our interim results on Form 6-K. We undertake no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this shareholder letter.

Rounding

Certain monetary amounts, percentages, and other figures included in this letter have been subject to rounding adjustments. The sum of individual metrics may not always equal total amounts indicated due to rounding.

Interim condensed consolidated statement of operations

(Unaudited)

(in € millions, except share and per share data)

|

|

|

Three months ended |

|

Six months ended |

|||||||||

|

|

|

June 30, 2021 |

|

March 31, 2021 |

|

June 30, 2020 |

|

June 30, 2021 |

|

June 30, 2020 |

|||

|

Revenue |

|

2,331 |

|

|

2,147 |

|

|

1,889 |

|

|

4,478 |

|

3,737 |

|

Cost of revenue |

|

1,668 |

|

|

1,599 |

|

|

1,410 |

|

|

3,267 |

|

2,786 |

|

Gross profit |

|

663 |

|

|

548 |

|

|

479 |

|

|

1,211 |

|

951 |

|

Research and development |

|

255 |

|

|

196 |

|

|

267 |

|

|

451 |

|

429 |

|

Sales and marketing |

|

279 |

|

|

236 |

|

|

248 |

|

|

515 |

|

479 |

|

General and administrative |

|

117 |

|

|

102 |

|

|

131 |

|

|

219 |

|

227 |

|

|

|

651 |

|

|

534 |

|

|

646 |

|

|

1,185 |

|

1,135 |

|

Operating income/(loss) |

|

12 |

|

|

14 |

|

|

(167) |

|

|

26 |

|

(184) |

|

Finance income |

|

21 |

|

|

104 |

|

|

6 |

|

|

125 |

|

76 |

|

Finance costs |

|

(25) |

|

|

(31) |

|

|

(294) |

|

|

(56) |

|

(306) |

|

Finance income/(costs) – net |

|

(4) |

|

|

73 |

|

|

(288) |

|

|

69 |

|

(230) |

|

Income/(loss) before tax |

|

8 |

|

|

87 |

|

|

(455) |

|

|

95 |

|

(414) |

|

Income tax expense/(benefit) |

|

28 |

|

|

64 |

|

|

(99) |

|

|

92 |

|

(59) |

|

Net (loss)/income attributable to owners of the parent |

|

(20) |

|

|

23 |

|

|

(356) |

|

|

3 |

|

(355) |

|

(Loss)/earnings per share attributable to owners of the |

|

|

|

|

|

|

|

|

|

|

|||

|

Basic |

|

(0.10) |

|

0.12 |

|

(1.91) |

|

0.02 |

|

(1.91) |

|||

|

Diluted |

|

(0.19) |

|

(0.25) |

|

(1.91) |

|

(0.44) |

|

(1.91) |

|||

|

Weighted-average ordinary shares outstanding |

|

|

|

|

|

|

|

|

|

|

|||

|

Basic |

|

191,172,946 |

|

190,565,397 |

|

186,552,877 |

|

190,870,850 |

|

185,799,600 |

|||

|

Diluted |

|

194,084,446 |

|

191,815,695 |

|

186,552,877 |

|

193,051,280 |

|

185,799,600 |

|||

Contacts

Investor Relations:

Bryan Goldberg

Lauren Katzen

ir@spotify.com

Public Relations:

Dustee Jenkins

press@spotify.com