Personal Entertainment For The Masses

The Race is On

By Andy Marken – andy@markencom.com

“It goes on. It goes on, Judah. The race… the race… is not… over!” – Messala, Ben-Hur, MGM, 1959

It’s probably best to think of 2022 as a recovery/realignment placeholder between 2020/21 and 2023 rather than an actual measurable period of progress.

The content creation/distribution industry spent most of the year realigning its long-range goals, perfecting and using their new tools/toys and trying to come to grips with the new facts of marketplace life in the year(s) ahead:

- There is a functional difference between movies and movies that award folks and theater owners are trying to qualify which will define the markets growth and profits.

- Linear/pay TV is living on borrowed time in developed countries with only modest growth in emerging countries.

- The streaming industry is focusing on a balance of realistic, profitable global growth, pricing ceilings (subscription/ad cost) and the cost of audience retention.

- There is a thinning of the content creation herd

Suffering from an overabundance of screens (more than 208,000 globally) and an under supply of “gotta see in a dark room with strangers” content, the theatrical industry teetered on bankruptcy until the middle of last year.

It was only the availability of a few long-awaited franchise tentpoles that made theater owners think survival, even prosperity, might be on the horizon for the greasy popcorn houses.

Tom Cruise’s Top Gun: Maverick hit the screens almost everywhere mid-year–with the notable exception of Chinese screens. That was followed by some decent seat-filling events. And with James Cameron’s Avatar: The Way of Water ending 2022, folks like AMC’s Adam Aron, Cineworld’s Mooky Greiding, NATO (North American Theater Owners) and other movie house owners gained faint hopes that the audiences would return … in droves.

It ain’t gonna happen!

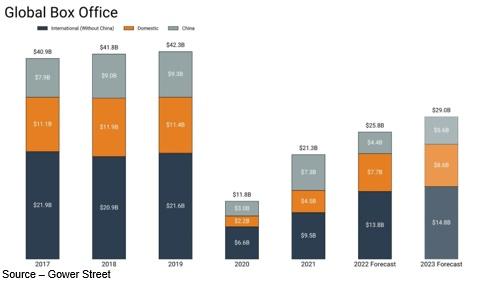

It’s true, 2022 ended with on theater owners worldwide bringing in an estimated $26B according to Gower Street…thanks to the tentpoles.

Modest Recovery – Movie theaters experienced good attendance last year, thanks to major tentpole productions, but they will have to adjust to “a new normal” in 2023.

Analysts project that 2023 ticket sales should increase to nearly $30B, up 12 percent over 2022. But that’s well below 2019’s $42.5B which has been part of shrinking movie theater attendance since 2012.

While the Americas are the largest ticket sales area – accounting for 40 percent of revenues – the second largest market (China) has almost literally closed its doors to U.S. projects.

Avatar: The Way of Water was one of the few American projects to be shown on the country’s screens. This helped Cameron hold three of the top five global earning spots. The other two were Avatar and Titanic.

Black Panther: Wakanda Forever and Top Gun: Maverick were both banned from the Middle Kingdom as Hollywood’s Chinese market share dropped from 45 percent to just about 8 percent this year.

China has been developing/refining its film production industry since 2015 but the pandemic moved it into high gear, delivering better and better films (we’re told) for the country’s audiences like The Wandering Earth and The Battle of Lake Changjin.

While the government and film approval organization allowed a minimum number of international projects to be shown locally to meet basic WTO (World Trade Organization) requirements, few of their projects are shown outside the country.

But there are signs that Chinese theaters may need Hollywood films more than studios need the Chinese audience. China’s screens are now just “nice to have,” rather than a necessity.

The problem for the global theater market is the fact that there simply aren’t enough door-busting projects to steadily fill seats and most studios also have their own DTC pipelines to fill.

Ttentpoles – $100M+ marketing – attract ticket buyers in droves but a studio can only afford one to two a year.

Few mid-range films of $30-$50M are made because it’s tough to second guess ticket buyers.

Lots of $10M+ projects are made because there’s a ready market for them – a limited theatrical window followed by posting on their own or other streaming service.

Yes, this is the year that DTC (direct to consumer) content delivery gets serious as pay TV continues its slow, mixed message slide into an entertainment afterthought.

Peak TV (day/time viewing) has steadily declined in the Americas from a high of 91 percent of the households down to 66 percent last year and will dip below 50 percent by the end of 2023.

Across the globe pay TV will continue to be strong – about 1B households – thanks to the penetration in developing countries of high-speed connectivity and low annual subscription costs.

To compensate for the steady subscription slide in the Americas; cable services slowly, steadily increased their monthly connectivity charges and increased their ad loads from 5 to 10 to 20 minutes per hour. In addition, they expanded their connectivity service for the household adding smart home services.

The bright spots for pay TV will be sport/live events, news and an aging population that is accustomed to regularly scheduled entertainment.

The increase in easy streaming support to Smart TV as well as the ability to use their streaming services across all devices – browsers, connected TV, game consoles, mobile and Smart TV – has encouraged Americans to shift and/or add three to four content services.

While Netflix started the streaming industry in 2007, followed shortly by Amazon, it took until the pre-pandemic to convince providers that the direct connection with the consumer could be the smart – and profitable – solution to the constantly rising charges of pay TV bundlers.

When Netflix and Amazon hit the subscription service ceiling in the Americas, they broadened their subscriber potential and content supply options in 190 countries.

Predictably with other tech companies and studios entering the race in the Americas, churn became the word of the day last year as financial and market analysts quickly realized households wouldn’t continue to sign up for new services regardless of the number they had or the total monthly cost.

To retain subscribers and profits, the previously ad-free subscription services determined perhaps the subscriber wouldn’t mind exchanging a little time – 3-4 min/hr. – for subscription cost savings.

Hybrid Growth – There are people who will prefer ad-free viewing and those who don’t mind a little intermission time. Getting up periodically is a good thing.

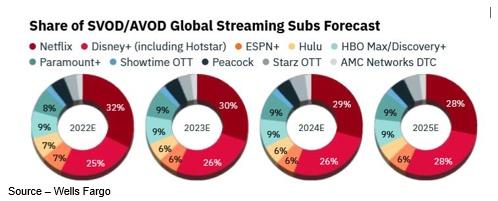

In 2023, SVOD and AVOD will become more intertwined as Netflix, Disney+, Paramount+ and Hulu fully address the ad market, the complexities of ad management/tracking and a shift in domestic subscribers’ interest in international content.

While they have tapped into global content since the beginning, we measure Amazon and Apple by different content/subscription guidelines than the other services. Not only are they global in reach, they have a range of personal/home services that buffers them from the ups and downs of the entertainment-viewing market.

Hybrid services has shifted the attention from monthly subscription numbers to ASR (average subscription rate) and weekly/content ratings.

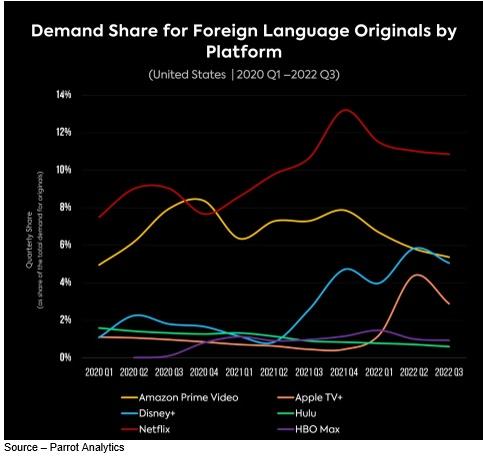

Foreign Fare – Netflix was the first to find out the benefits of the requirement to produce 30 percent of their content locally and stream it to customers around the world. It gave viewers everywhere inexpensive, new, unique stories.

The program ratings are one of the key reasons Netflix continues to be the most widely recognized service and the last one subscribers said they would drop for another service. The platform consistently dominates the top foreign-language streaming originals list, with 8 out of 10 shows.

A steady flow of such shows as Somebody, Spirit Rangers, Missing, Arcane, Kipo, Cyberpunk, Bridgerton, Stranger Things, Squid Games, Kaleidoscope, Vikings, Beef and a range of new films/shows from Japan, South Korea, Europe and most recently Africa have given Netflix, Disney, Amazon, Apple and Paramount a breath of uniqueness and consumer demand.

That internationally created content will account for more than 18 percent of consumer demand in the Americas this coming year, compared to only 8 percent in 2022

With Iger returning as CEO of Disney, the company will reprioritize its creative content development/delivery, surpass Netflix global subscribers and develop a more solid/focused path to tomorrow.

And yes, Iger and the board will tap and train his replacement for the years ahead.

Perhaps most important will be the company’s move to finally bring Hulu fully under the Disney umbrella.

The time is right for Comcast, the world’s largest cable/broadband service provider, to sell Disney their 30 percent ownership of Hulu so they can focus on more fertile opportunities.

This will give Comcast’s boss Brian Roberts the freedom to buy some – if not all – of Warner Bros shattered pieces, showing the FCC that the rescue will be in the best interest of the industry and the consumer.

For the past two years, WBD’s David Zaslav has been focused on reducing/hopefully eliminating the huge $50B debt he inherited by every means necessary – content impairments/write-offs and staff termination costs – while justifying his modest $246M annual compensation.

About the only segment that hasn’t gone untouched has been Discovery’s reality fix-em-up, cooking projects, which have been inexpensive, popular, profitable.

A firm believer in Jack “Sledgehammer” Welch’s business techniques, his improvements have included wide

and deep staff, team, project cuts at Warner Bros; shedding/retiring films/series from HBO/Max and marginalizing of CNN shows and news gathering.

Zaslav tapped the team of James Gunn and Peter Safran to disassemble and rebuild DCEU (DC Extended Universe). This included the shelving/shutting down of nearly all pre-Zaslav titles/projects and developing a comprehensive 10-year plan to make DC the center of the superhero universe.

The plan must be good because Gunn assigned the first major project – the reimaging of Superman – to himself to write.

Out of the rubble, Roberts sees potential for Comcast, NBCUniversal, Sky and a major boost for Peacock streaming.

By 2024 (just around the corner) Zaslav will be free to “consider” transactions, and the content world will be ready for a pleasant change.

2023 is going to be … entertaining!

Andy Marken – andy@markencom.com – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. Internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields. Extended range of relationships with business, industry trade press, online media and industry analysts/consultants.