People Really Want Better Bundled Entertainment

Content Insider #861 – Unseen

By Andy Marken – andy@markencom.com

“Well, maybe I overshot a little, because I was aiming at just enough to keep you from walking out.” – Melvin Udall, “As Good as it Gets,” TriStar Pictures, 1997

We never watched 90 percent of the stuff available on our cable bundle but never secretly thought about dumping it because of the 10 percent we did watch.

There was some order to the world because we knew we had an appointment with the set Tuesday evening at 9 p.m. to watch the next chapter of some series.

Oh sure, the bundle fee would go up predictably but …

Over time, the number of ads during any given hour became so frequent we were certain they were breeding in the bundle.

Today, the result is a two-tier industry which the industry itself created.

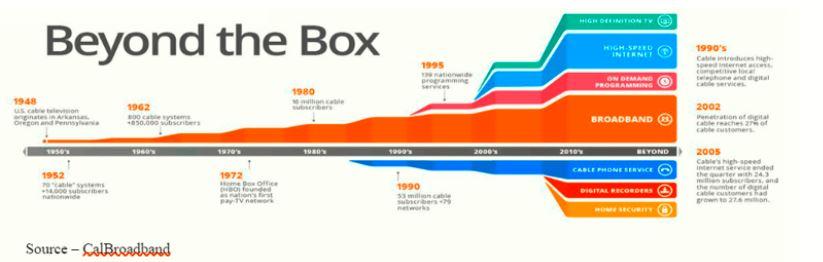

Broadband Evolution – The internet grew on the back of cable (increasingly, fiberoptic) that spans the globe and connects to nearly every office/home. Both cable and telco companies now deliver voice and video content over the connection to your home. That connection is vital whether the household has a bundled pay TV or streaming home entertainment service.

The cable bundle was born out of necessity – networks needed to put their services/wares in front of the maximum number of households and consumers wanted/needed a simple way to pursue their viewing options.

Households around the country and the world were embracing broadband service to their homes for internet connectivity.

Instead of searching through five, 10 or 20 OTA (over the air) channels, broadband services (cable companies) offered a fast, easy solution to satisfy both parties:

- Broadcasters and specialty content folks had fast, reliable access to the home and its TV(s). Today, nearly 98 percent of US households have broadband access and globally nearly 1.5B of an estimated 1.75B households have access

- Consumers have a bundle of home entertainment options with a single interface to scan and select shows/movies from the various providers including news, a range of series shows, games, contests and … sports

TV Time – Networks and local stations launched news and entertainment shows over the air and over the net. And to make it simple to find what you wanted, they developed scheduled appearances of shows/programs so everyone in the house huddled around the set knowing what they were going to watch.

It was great–everyone had what they wanted:

- Folks at home had instant access to the shows, content they wanted

- Broadcasters could focus on creating, acquiring great content, building a viewing audience and household counts to sell to advertisers

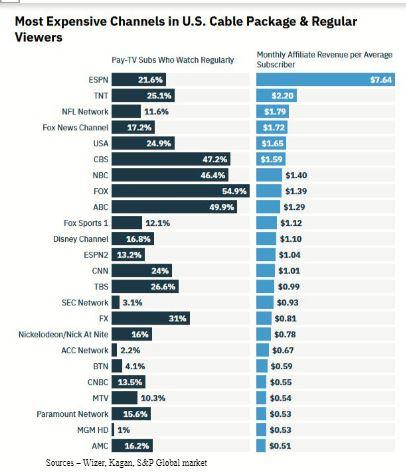

But the fledgling ESPN – now part of Disney – had a product that everyone (okay, 20 percent of the subscribers) wanted – sports – and they needed money to survive.

The solution was a carriage fee that all of the subscribers would share on top of their TV connection to have instant access to the sports whether you watched or not.

While other services had/have larger audiences, ESPN had a significantly larger annual payout to the various sporting associations, organizations, activities.

So, their carriage fees grew while other services in the bundle – even those content services that added sports to build viewership – remained “reasonable,” making up the difference on the other end … ads based on their reach and viewership.

Carriage Fee – You can probably thank early moves by ESPN for your constantly rising bundled pay TV bill. In return for being a part of the bundle (and important to a minor segment of the population), they demanded – and got – a special carriage fee to supplement their ad income. Despite their growing financial health, it’s tough to wean them – or any network – off the fee, even though you’re not a sports fan/fanatic.

Now, while most folks might not be a part of the sports fan crowd except for one game a year and spend the majority of their viewing time on four or five of the entertainment channels, the cable guy simply points out that it is all there for you to enjoy.

It was a good deal for nearly everyone – the cable guy, the network/content provider – except for the viewing household because the carriage fees never go down, even if viewership slides.

But it’s too difficult for them to break from steady cashflow to venture out on their own unless they’re starting from scratch.

So, you can thank/blame Netflix for changing the industry and the way the game is played.

It wasn’t really a giant leap for Reed Hastings and his crew.

Breaking Tradition – Netflix has been credited/blamed for encouraging people to cut their cable bundle and choose the service they want to watch, when and on the screen they want. The move for them was to reduce costs and speed service by dropping the red envelope disc delivery and using the internet for content distribution.

They were already in the content rental business, sending film/show discs through the mail.

All they really did was cut out the middleman and send folks their content in a better, faster and more economical fashion … over the now reliable internet.

Folks who never paid the constantly increasing bundle fee and were born on the internet loved the idea – watch what you want in their library when you want instead of waiting a few days for a red envelope to arrive.

Chicken Soup (owners of Red Box) did try to buy the mail order business, but the customer base was too important to share so …

With the internet at their disposal, Hastings and his new cohort, Ted Sarandos, set their sights on the global home entertainment market, not just Millennial and Gen Z people US who never had a cable bundle.

They built a global content production/distribution network with video stories being produced in more than 190 countries.

You know, really different stuff, new/unique content; not a spin-off of a spin-off or resuscitation of an oldie but goodie or another franchise extension.

People liked the idea of watching what you want, when you want, on the screen you want for the monthly cost of a couple of cups of coffee and oh yeah, no ads.

Of course, they would change their no ad position later but …

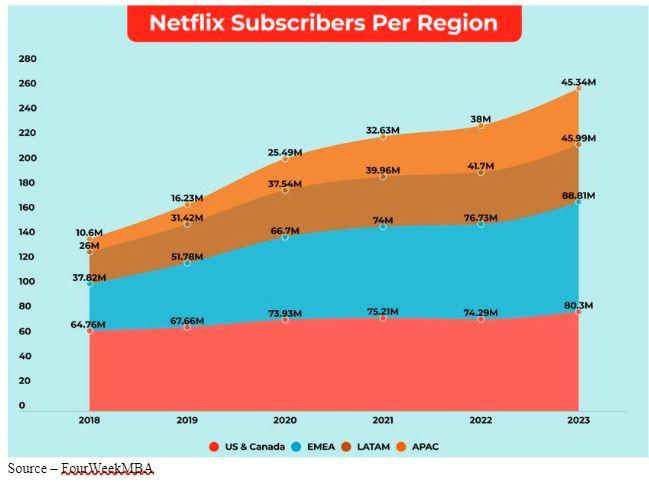

Global Reach – By developing their own shows/movies and licensing them from networks and studios in the US and around the globe, Netflix has become the largest streaming video service and the most profitable.

Netflix – which network/studio folks were sure would go broke, not only attracted new viewers/subscribers around the globe but also started to make money.

Who knew an hour movie could actually be an hour long!

Amazon with their global customer base (230M customers) who were already ordering stuff from them over the internet in Timbuktu, Melbourne, Mumbi, Zagreb, Lagos and beyond, figured another service in their catalog was a worthwhile investment.

Apple, with nearly 1.5B folks around the globe using their beloved devices and all kinds of Apple apps figured adding films/shows wasn’t a big reach for them.

Fast Riser – Pay TV subscriptions have dropped to less than 50 percent of the households in the Americas but remain relatively constant around the globe. Today, more than 200 streaming video services also vie for viewers’ time and subscriptions.

While the cable bundle business remained relatively constant – shrinking slightly in the Americas but continuing to grow slightly in the ROW – Igor and the rest of the studio/network heads saw future growth rested with the younger audience.

After all, they know content better than the upstarts so they could keep their bundled service cushion and invest in the younger generation of viewers.

The problem is the subscriptions aren’t as predictable with their streaming service because people sign up, watch the stuff they want and leave to enjoy the next guy’s fresh new content.

The constant in/out churn was about 50 percent last year, according to Parks Associates.

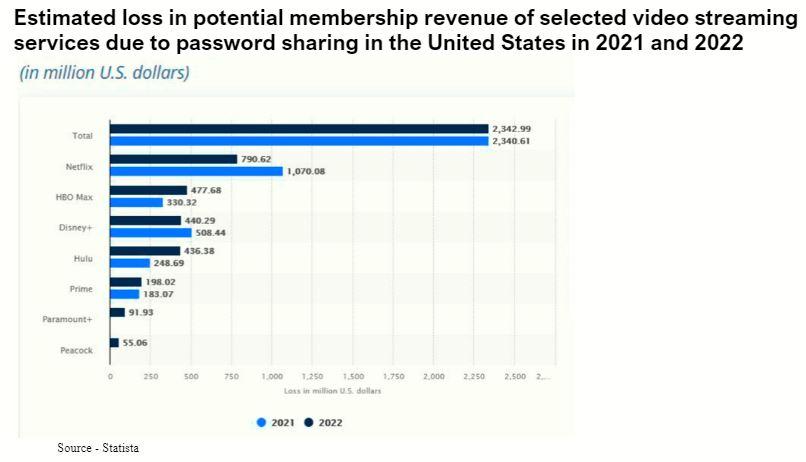

In addition, what Netflix neglected to tell the studios/networks who were building their own streaming audiences was that while the viewership numbers looked mouthwatering, not everyone was really a subscriber and sharing passwords was becoming increasingly expensive.

Recovering Revenue – All of the streaming video services suffer from lost revenue when people share their service passwords with others. Netflix was the first to try to end the losses by getting tough with subscribers and offering a number of different streaming service options/prices. Despite a momentary dip in subscriptions, subscribers returned and slowly, the other services have cracked down on sharing. It may never be 100 percent successful, but every paid subscription helps.

Netflix was the first to say enough is enough and announced they were going to crack down on freeloaders but would offer them an option – a lower monthly fee service that would be subsidized by a few ads – three to four minutes per hour.

Network and studio bosses as well as Wall Street were certain the low cost, limited ad option would crush Netflix growth. It did result in a few quarters of less than projected increase, but viewers returned because they had options in addition to an increase in the depth and breadth of content available to them.

D**n!

Disney continued to invest in new content, added an ad-supported option to their service, got tough on password sharing and experienced similar results.

While the others quietly did the same, WBD which has been constantly rearranging service groups, content and people was the last to publicly say they were going to do something new, bold and different … crack down on password sharing.

Searching – The biggest problem/frustration for people with multiple streaming services is to locate the show/movie they want by wading through application after application and often “settling.”

The one issue that has dogged all of the services (in addition to a steady increase in subscription fees) is the consumers’ growing frustration about the inability to quickly, easily find the show/movie they want to watch.

The answer was simple for the content service experts … they invented the bundle!

Disney took all of the best of their stuff – Disney+, Hulu, ESPN+, Marvel, Pixar – and put it all in one slightly expensive package.

WBD rolled out their totally complete bundle – Max (HBO), TNT, Discovery, CNN, Turner, more – of content that will meet “everyone’s entertainment desires.”

Discussions are still going on about Paramount and Peacock coming together as a fresh, new streaming solution either through acquisition or joint venture.

Oh yes, to increase their overall profits, they’ve determined they should license some of their older but highly popular shows/series to Netflix – the big dog in streaming – which have enjoyed renewed audience interest/attention.

The result is a fantastic array of streaming walled gardens.

The problem is they are all self-serving bundles.

Okay, to give them credit, Verizon has made a foray into offering a streaming bundle.

In addition to broadband service, they are offering customers Max and Netflix at a special price.

It could be/should be the beginning of a bundled entertainment service that would give the broadband services a boost, a little more subscription stability for the streaming services and entertainment variety that the cord nevers have been looking for.

Home Pipe – The broadband service – wired and wireless – is already in service in the Americas and other countries, and they could provide consumers an added entertainment option of tailored bundles of streaming services. Economic and easy to find/view content would be a great service.

Spectrum, still a major bundled service provider, also reached an agreement with Disney to offer their streaming services to customers at an equally “reasonable” cost.

With landline phone service shrinking faster than cable bundle subscriptions, cable/broadband services can provide consumers two flavors of entertainment – a predictable day/date entertainment service and a streamed bundle of anytime entertainment bundle, including multiple streamers.

The broadband streaming bundle could meet most, if not all, of the younger cord never entertainment requirements with subscription/ad free or ad-supported options as well a free ad-supported services like Tubi, Pluto and FreeVee.

Understand Us – We understand that every streaming, broadcast service and studio is certain they have exactly what consumers want to view; but if they would sit on the viewer’s side of the screen, the needs might be even more simple than their greatness. All services have to do is … listen.

In addition, and perhaps most importantly from our perspective, it would cut out the new emerging middleman – the connected TV folks like Walmart with their Vizio sets as well as manufacturers such as Sony and LG that view the home screen as another way to monetize the consumers’ data by selling ad time on their customers’ screens.

The broadband services already connect to over 90 percent of the entertainment-ready households and are adding wireless services so it’s really a small step for them to become an easy-to-live-with and understand solution … a full-service communications and entertainment provider.

The pay TV bundle continues to provide customers with everything they presently enjoy as well as the occasional impulse-viewing option they click on when they’re surfing the day/time program guide, DVR capability and predictability.

The streaming bundle can be tailored to the people mix of subscription and ad-supported services that meet their budget and viewing interests.

When it comes to their entertainment enjoyment, people today are beginning to agree with Melvin Udall in As Good as it Gets, when he said, “I’m drowning here, and you’re describing the water!

It’s difficult enough for a bundle TV user to pick a couple of shows/movies they want to watch from the vast array of channels available on their screen.

Adding 200 streaming walled gardens to search in and out of is more than even our Gen Z folks want to face just so they can escape the reality of today’s world.

The pipe to the household and consumer is already there.

Now all we have to do is figure out how to make it really useful – and profitable – for folks who create, bundle and view the content.

Andy Marken – andy@markencom.com – is an author of more than 800 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.