Movie, Show Folks Need to Recognize, Address the Total Market

Content Insider #816 – Blended

By Andy Marken – andy@markencom.com

“Bheem, you have taken me closer to my ambition. You’ve given me this attire that will inspire me through this quest.”—Alluri Starama “Raju, RRR,” DVV Entertainment, 2022

The best thing that has happened with the home entertainment market in the past 16 years was when Netflix and Amazon announced their streaming video services.

Like a boulder rolling downhill, people liked the idea of watching a movie or original project now caught on–especially without 20-minutes of ads every hour and a reasonable monthly price – $4.99.

It’s true, Amazon Prime was more expensive, but you got all that free shipping for stuff and nothing’s better than free.

That streaming video jumping off point was also the worst thing that happened to the home entertainment market.

Suddenly, every studio and TV network saw an opportunity to go directly to the consumer (eliminating paying the cable guy) and developing a long-term, profitable relationship.

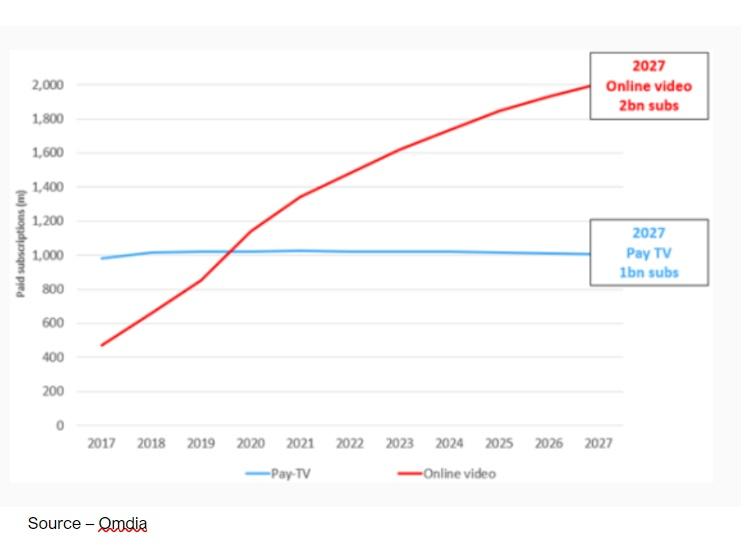

Global Views – Streaming video has quickly become the home viewing entertainment option of choice in the world while pay TV has ceased to grow or maintain its subscriptions in emerging markets and with older generations.

Fast forward to today and pay TV popularity has dropped in industrialized countries – bolstered only by emerging countries – while streaming has shown significant growth.

There’s a mind-boggling list of “outstanding library and new/unique films/shows” with offerings from more than 200 streaming services – SVOD, AVOD, FAST–each with their own subscription pricing formula, depending on how valuable – and vital – their content is to your household.

While pay TV has reached what FX boss John Landgraf calls the year of Peak TV (decline of subscribers and decline of real shows, scripted stuff) reality, game/contest doesn’t really, count right?

According to Nielsen, consumer interest in streaming ballooned with more than 19.4M years of content watched last year, up from 15M years in 2021.

Creative Investment – Despite the creative strikes in the U.S., studios and streamers are continuing to invest in new, unique content to attract and retain subscribers. Where investments will be when the dust settles is uncertain.

But management has shifted their priorities from more viewers to more profitable viewers.

“Streamers and studios have realigned their investments in new movies and series in order to grow their pipelines and entice more streaming subscribers,” said Allan McLennan, president/CGA, 2G Optimization.

“They are focusing on ARPU (average revenue per user), with the investment still being significant.”

“How the writer/director and other guild/union strikes in the US will affect that investment in the U.S. depends on the duration of the standoff,” he continued. “However, content development and production investment are still moving forward in other countries.”

“The demand continues to grow,” he added. “Original content is the competitive advantage every streaming service leans into/promotes because it attracts people to the platform.”

But is that enough to get and keep people onboard?

More than 450M households around the world paid an estimated $99B last year for their content without advertising. Digital TV Research projects that this expenditure will increase to $124B by 2028 and U.S. households will lead the ad-free subscriptions, spending an estimated $25B by then followed by second-place China.

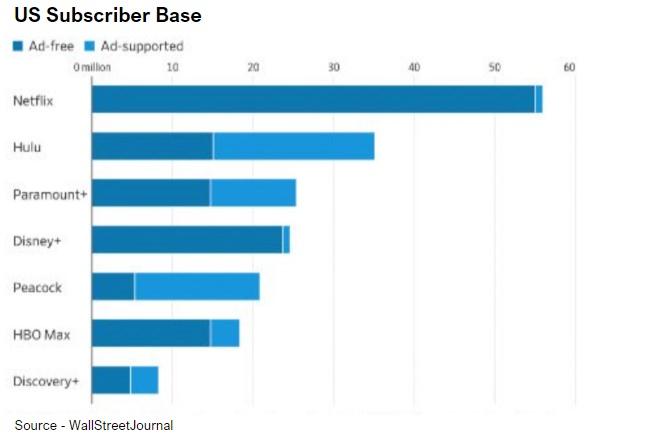

Even with its addition of an ad-supported option, Netflix is thought to continue to be the leading SVOD service followed closely by Amazon Prime and Disney +/Hulu.

WBD has a lot riding on its Max bundle and are counting on their Discovery loyalists to provide a base while new projects attract new subscribers even as their churn continues. Their challenge will be their start/stop activities internationally and understanding that they need to be more aggressive beyond home-grown and superhero projects.

Paramount + has gained a strong and increasingly profitable number four position but its international presence is minimal compared to Netflix and Amazon Prime subscriptions and project production everywhere but Russia, North Korea, China and Syria.

Peacock, owned by NBCUniversal/Comcast, will continue to focus on its home, U.S. market with an aggressive $20/yearly fee to attract subscribers and its parent dwindling pay TV user base. In the Americas, they parallel mobile phone services, fighting over the same audience.

Streaming services are slowly beginning to understand that consumers don’t have a bottomless home entertainment budget and they don’t really hate ads. They turn off when there are 20 minutes of ads in an hour of entertainment, and they tune out dumb and repetitive ads.

To beef up their subscription numbers, streamers have added ad-supported options and are theoretically bundling their services.

The ad-supported options are attracting the subscribers but are only slowly attracting marketers who are having a difficult time understanding and coming to grips with the value of reaching the right customers with the right message rather than thinking in terms of CPM (cost per thousand).

Budget Management – Households are taking a closer look at which services they have to have without ad interruptions and those that are occasionally used and are tolerable with a few ads. Value will play an important role in people’s decisions going forward.

It will take the second oldest profession in the world a while to understand, interpret and use the tremendous data bases of detailed subscriber information the streamers have accumulated to understand that personalized marketing really has to be … personal.

That’s not a condemnation because even the streamers have a tough time when they add and drop projects from the library with frustrating regularity. Millions of folks finally “get into” a film/series only to see it being replaced.

Even though folks are happy with “status quo,” sometimes you just have to plan for/anticipate change.

Of course, the studios and networks have a solution for the consumer … their solution.

Bundles are a move in the right direction, but the problem is it’s their bundle.

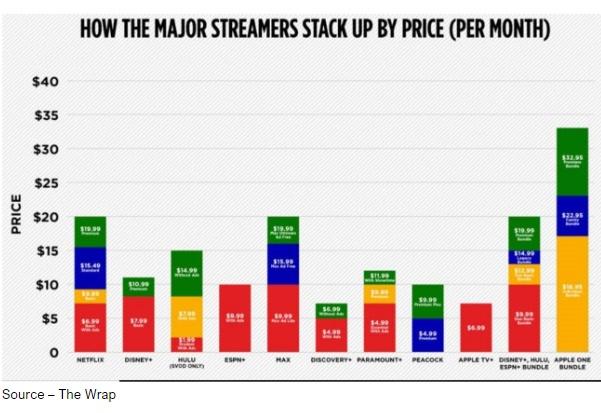

Tiers – All streaming services have shifted to some form of ad-supported and ad-free options except for Apple which is focusing on addressing much more of the viewer’s interests.

Disney has its bundle (Disney+, ESPN+, Hulu) and WBD has their bundle (Max, CNN, Discovery, Turner Sports, Cartoon Network and WB films).

Both moves are good but even WBD’s CFO Gunnar Wiedelfels admits it’s probably not enough because there are times when you want to watch a show/movie that Lionsgate, WBD, Paramount, Sony, Universal, Disney, Netflix, A24, or one of the other indie projects and it’s not available in the bundle you happen to subscribe to.

The best solution to enjoying a movie or series is to go back to your old pay TV bundle.

But nobody is willing to put up with the ever-increasing bill, restricted day/hour viewing and contract hassle.

As our dad used to say, “That dog don’t hunt anymore.”

“In a relatively short period of time, streaming video has become an accepted way consumers get their entertainment,” McLennan noted. “Watching what you want, where you want, when you want and on the screen in front of you has become the accepted norm.

“Nearly half of the households in mature markets use it regularly. That level of usage will soon become the standard in the rest of the world,” he said. “But ultimately, the industry will have to yield to the consumer’s demand for a single, personalized entertainment portal.”

Heck, we’ve been saying that all along and FAST bundles seem to be a step in the right direction.

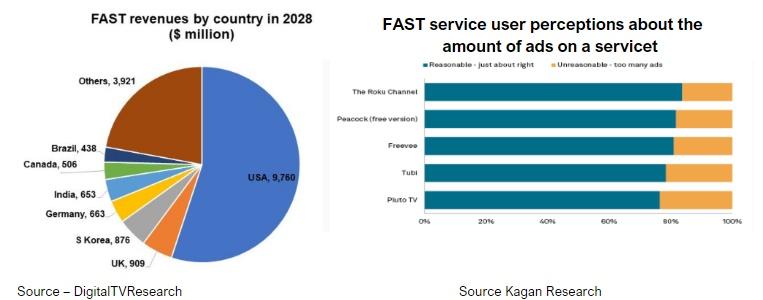

Great Option – People are quickly determining one of their best video entertainment options is one that is free (with ads) and provides a wide range of film/show choices. The number of ads is okay, but several services need to be more thoughtful as to when and where the ads are inserted.

Increasingly, they offer a growing breadth of genres that appeal to young and old, and the present balance of ads vs. content viewing is acceptable for most people.

Last year, ad-supported viewing options accounted for about 32 percent of the premium subscriptions.

Analysts at MoffettNathanson suggest that ad-supported service subscriptions will continue to expand at the rate of 25 percent per year compared to ad-free subscriptions which will grow at less than10 percent per year over the next few years.

We aren’t naive enough to think that the ad vs. entertainment ratio won’t change as the FAST channels become more popular and are used by a broader audience.

If studio streamers are really serious about “replicating the cable bundle,” without all of the negatives, participating with the FAST services could be what WBD’s Max chief Casey Bloys, observed, “makes economic sense.”

Okay, he really meant everyone else doing it with their service; but why reinvent the wheel?

It still won’t eliminate the frustration of finding that specific movie or show you want to watch now, but it couldn’t hurt.

Or there could be times that you’re like us and really don’t care. You simply want to watch a good horror sci-fi flick or mindless romcom drama. They certainly have the personal data and software tools (AI) to give you some viable options for you to waste an hour or two watching.

Take That – Most streaming viewers find their biggest challenge when sitting down to enjoy a movie or show is finding just which video story they’re really interested in spending time with. It can be … difficult.

Even if the service(s) don’t get it right, you can always count on your friends, passing acquaintances or folks on social media to give you recommendations and advice … even when you don’t ask.

The major problem with the new entertainment freedom of streaming video content really isn’t the cost (important, yes but …).

Instead, there are just too d*** many of them.

A Little Help – While you may be a little confused on what movie/show you want to waste a few hours on, you can always count on someone to tell/show you which viewing option is best.

To help us go through the morass of films/shows, we use JustWatch. It helps us wade through the premium and ad-supported services. It tells us what’s new and popular/trending in addition to letting us skim projects like genre. It even gives us a place to keep our “wanna see this” list.

It’s not perfect, but it does save a little time/frustration.

Across the Americas, households had roughly the same number of premium video sources (6.1) last year.

The breakdown of ad-free and ad-supported services will be about 50/50 by the end of the year, according to MoffettNathanson.

Budget is a factor in people’s ever-shifting decisions, but the perceived value will be more important than cost.

Depending on the household make up – single, couple, children – “go to first” service selections will vary.

Those that are used less frequently or by chance won’t be “worth as much,” regardless of the quality of the films/shows that are available.

McLennan explained that today, consumers have probably signed up for more video sources than they need, but they keep them because it is too complex to find a show/film that they really want to sit back and enjoy.

And with more than 200 streaming services available, that makes it extremely difficult for the majority of services to rise to being really profitable.

The best move for independent producers and streaming services is to get onboard with one or more of the volume content FAST services to free themselves from the important backroom technical work and concentrate on the important project/service marketing and promotion activities.

We recently took a step back and realized that most of the streaming services are ignoring/overlooking big portions of their markets.

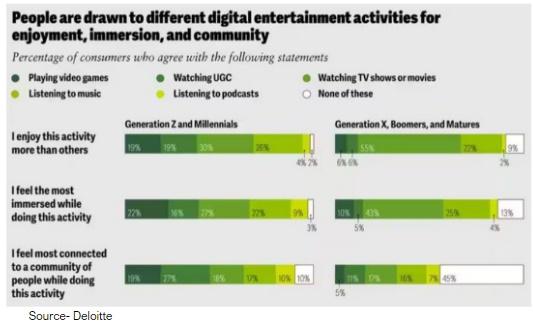

Folks who were born with a screen and controller in their hand are less dependent on video content.

Their online interests/activities are more diverse– gaming, social media, podcasts, and individually produced short videos – YouTube, TikTok, etc.

Take a look at the major streamers/price chart listed earlier.

Apple does a pretty good job of selecting the movies/shows they acquire for their Apple TV+ service such as CODA, Ted Lasso, Shrinking, The Last Thing He Told Me, Silo and a steady stream of award-winning/award- worthy projects.

After all, they have those iPhone, iPad, Apple Watch and Mac users/loyalists who have come to expect a protected environment where they really have a personalized option bundle.

Apple One gives those folks added stuff they want – Apple Music, Apple TV+, Apple Arcade, iCloud+ (siloed storage), health/fitness and well, just about everything.

Cripes, all of the other streaming services would probably fire huge chunks of their workforce to spend on those video stories … ooppss, they already have!

The only one that comes close is Amazon with all of their services laid on top of free shipping.

Back when Netflix’s original co-CEOs (Hastings, Sandandos) announced their video game program, Wall Street and video market analysts said they were losing focus.

Those “experts” said Netflix needed to focus on great video stories for Gen Zs and Millennials (and older folks too).

They ignored the fact that these folks also like to play video games, watch UGC (user-generated content) and do other stuff out in the connected world.

The best way to keep folks and enhance your ARPU is to be first to deliver more entertainment options.

Movies/shows bring them to the service.

But they also play/participate in a wide range of games.

Younger generations – Gen Zs and Millennials – play video games to be entertained but also for social connection and a sense of immersion.

You know, that feeling of being deeply engaged and even transported into the screen.

That’s why last year:

- 3B+ people were active video gamers

- The market is estimated to be worth $197B

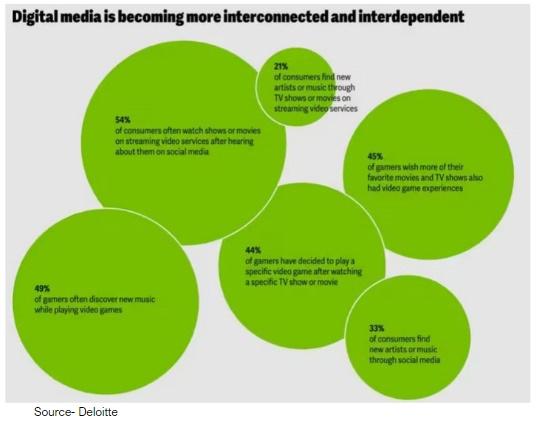

Multiple Interests – Video content creators seldom think people can/should satisfy all of their entertainment needs with their productions and only give passing acknowledgement to the fact that there is more – much more. Sharing entertainment ideas across the spectrum enriches viewing and production.

Since we’re not much of a gamer, our friend Mark, a dedicated game and film analyst/critic, helped us see that the line between the two were blurring.

Dungeons & Dragons, Super Mario Brothers, Fortnite and more have been tremendously popular games that set the stage for equally successful films.

Films/shows like The Last of Us, Suicide Squad, Star Wars, Avatar, Lord of the Rings have become go-to games.

He reeled off a lot more titles from both sides of the creation world, but we got the picture.

In other words, there is a cross-over between video stories and games.

People want all types of entertainment, and they want it all in one place.

Discovery – People find entertainment almost everywhere and the content creators who can produce materials that span the spectrum continue to increase their value to viewers, consumers, users.

As Bheem said in RRR, “We shouldn’t be scared anymore, we should surge forward.”

The best way to do that is together.

It’s important for all entertainment providers to anticipate where their audiences will be in the future.

Andy Marken – andy@markencom.com – is an author of more than 800 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.