Despite Successes, Streaming Needs Work

Insider #803A – Calculated Risks

By Andy Marken – andy@markencom.com

“Sometimes you get the pinball machine, and sometimes the pinball machine gets you.”, Roger Sharp, Pinball: “The Man Who Saved the Game,” MPI Original Films, 2022

Lots of folks at NAB said the industry has shifted. Suddenly, it’s all about streaming.

Not necessarily so!

Right now, it’s messy, which is exactly how the industry makes progress.

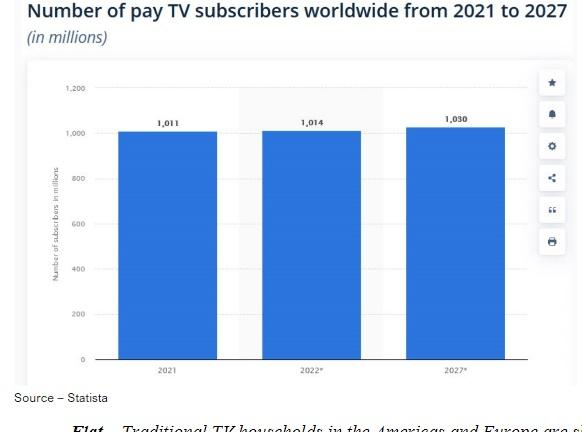

Bundled TV (Pay TV) isn’t dead. It’s just the same ol’ game. Not a lot new, not a lot anyone can do to influence how quickly it grows, plateaus.

And there certainly aren’t, at least for now, any new, exciting players shaking things up.

Flat – Traditional TV households in the Americas and Europe are shrinking in numbers as people switch to anytime, anyplace, any content (nearly) streaming options. Growth is only modest in emerging countries where service is inexpensive and plentiful.

The subscription-based services provide bundles of 200 +/- appointment TV channels of entertainment, news, sports and a crap load of ads (20 minutes worth every hour as an average) to a shrinking audience in the Americas and Europe.

However channeled bundles (cable, satellite) are finding new customers in developing parts of the world.

Revenue dropped nearly $50B over the past two years, even as the subscription base clawed its way to slightly more than 1B customers.

Reality shows (cheap to produce), news, sports, a sprinkling of new/long-running series (with decreased budgets) and habits are keeping people connected.

If – and when – streaming services begin investing in news operations and sports, they will chip away at the local, regional and national Pay TV numbers.

Still … the cable, satellite, wireless folks will persist.

People need the infrastructure service these folks provide for streamers and consumers.

“Don’t count them out,” said Allan McLennan, global head of PADEM Media Group. “They have invested heavily in a solid regional, national and international infrastructure that streamers and screen viewers need.

“Firms like Comcast also have pay and streaming – NBC and Peacock – that give viewers screen/time flexibility,” he explained.

McLennan noted that financial and industry analysts are overlooking the fact that Pay TV/infrastructure providers can also become major players in the streaming entertainment arena by rolling out their own Fast TV bundles.

That might eliminate two of the biggest complaints cable-cutting streaming viewers have–content selection confusion and budget management.

“They don’t really have hardening of the arteries,” he added.

But Netflix flexed its muscles during its quarterly earnings report made mid-way through NAB, adding 1.75M subscribers compared to a surprising loss in Q1, 2022.

Growth was back and streaming leaders were quick to reassure financial, industry analysts and shareholders that despite the potential strike of the WGA (Writers Guild of America), the streaming market would continue to grow.

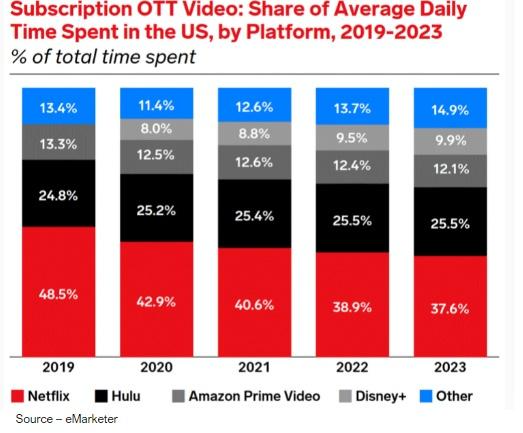

It’s Global – The seven leading streaming service providers in the US are aggressively focusing on capturing viewers around the globe having found that good video stories don’t suffer from national borders.

Netflix’s Sandaros and executives with the other leading SVOD services (Disney +, Amazon Prime Video, Max (WBD), Hulu, Apple TV+ and Paramount+) all said they are hoping for a fast resolution to the contract discussions and were working hard to reach “an equitable solution.”

But they are also well prepared to move forward.

They’ve developed/acquired large libraries of projects they can reformat, localize and quickly distribute in-order to rotate in/out of the lineup and even refresh films/shows, if necessary, to keep subscribers connected, involved.

They have all focused on expanding their content acquisition and subscriber base outside the Americas to offer a greater variety of movies/shows.

The leading studios/streaming services in the US are buying movies/shows from international content developers and have increased their investment in project production in Europe, APAC, Middle Eastern and Africa. This provides access to content in multiple languages presented whether in their original region of production’ or localized to be viewed and engaged.

Relatively Flat – The major streaming services in the Americas are maintaining their places with households as most average four services which is why the leaders have shifted their attention on Asia, Africa and Latin America. The shift also provides them with quality regional films/shows to offer to folks in other countries.

McLennan said the shift in focus is because 89 percent of US households have at least one streaming service and an average of four services (SVOD, AVOD, FAST).

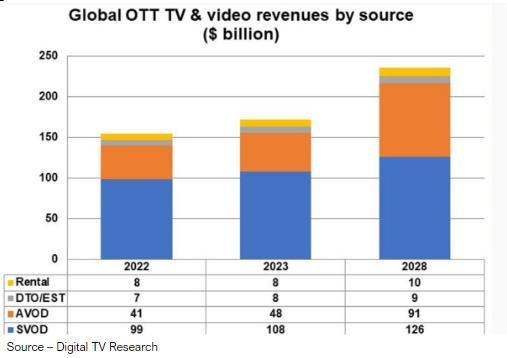

According to Digital TV Research, the global AVOD revenues to reach $91b by 2028,

In addition, services are moving from subscriber growth at all costs to what really counts, ARPU (average revenue per user).

Sarandos noted that Nielsen reported that Netflix accounted for 10 percent of total TV viewing in the US, making the company the most viewed streaming service/broadcaster in the country.

Living in Silicon Valley, we’re often accused of having a distorted view of what “everyone does it” – a third of the folks drive Teslas, everyone has a couple of iPhones, and people have a constant schedule of Zoom meetings.

You too, right? Right??

By focusing on ARPU, subscriber growth could produce $3.5B in free cash flow annually for Netflix, especially since they have subscribers and film/show production relationships in more than 190 countries (excluding Russia, North Korea, Syria, China, Crimea).

Ceiling – Video streaming services in the Americas and Europe are approaching the point where subscriber acquisition has to come by offering lower-cost streaming options, taking customers from other services or hoping folks will simply increase their home entertainment budgets.

The global shift has also been beneficial for Disney+, Amazon Prime, Apple TV+, Hulu, WBD and Paramount.

Current leading global streaming services are:

- Netflix (232.5 million paid subscribers)

- Disney+ (164 million paid subscribers)

- Amazon Prime Video (117 million paid subscribers)

- Max (48 million paid subscribers)

- Hulu (47 million paid subscribers)

- Paramount+ (46 million paid subscribers)

Apple TV+, which just happens to be part of a much larger (and profitable) hardware/software organization, has been slower and more cautious in its growth. The company has an estimated 20-30M subscribers (6 percent market share) with a measured increase in quality movies, TV series and live events as well as its MLS (Major League Soccer) relationship.

But…

There was more interest in streaming’s move to tiered service offerings, including AVOD.

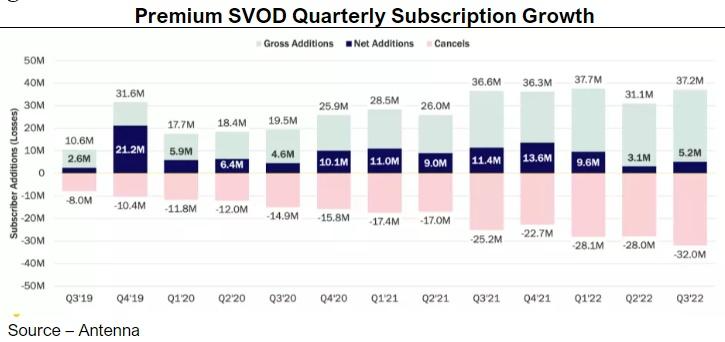

Back ‘n Forth – Churn means dropping one streaming service, adding another and later returning – but mobile phone services switched from quarterly cycles to ARPU and so will the streaming entertainment folks.

Churn or “subscription fatigue” among consumers is only getting worse, making it even more challenging for direct-to-customer video providers to retain customers.

According to Deloitte’s 17th annual Digital Media Trends report released during NAB, US consumers were paying on the average of $48 per month for their subscription-video services, plus the cost of their wired/wireless connections.

The consensus was they “pay too much” for SVOD services.

A third of the households said they intend to reduce the number of entertainment subscriptions or move to less expensive options.

While the rate of inflation has outpaced entertainment’s price increases but with fixed household costs rising for fuel, food and housing, people are taking a closer look at their discretionary spending.

Deloitte found that nearly half of the consumers (47 percent) surveyed said they have or planned to cancel a paid service, switch to a free ad-supported version of a service or move to a bundled service.

McLennan noted that often a household’s churn – cutting one service for another – was temporary as people would renew the service in six months.

“AVOD and FAST services will show the greatest consumer subscription growth this year, but it will take time to see how much it impacts the SVOD subscription base,” he commented. AVOD and FAST can help provide TV retain viewers with an economic path as it is an evolution of what ad-supported television has always been, IP targeting to viewers, on any device anywhere due to IP delivery.

“In many ways, this is very much what those of us experienced a number of years ago when premium television programing was introduced i.e., HBO/Showtime. A very similar transition then as perhaps today due to audience demand. But it certainly is an evolution due to the delivery and engagement efficiencies than a disruption which can be beneficial in many ways–especially with gaining new audiences.

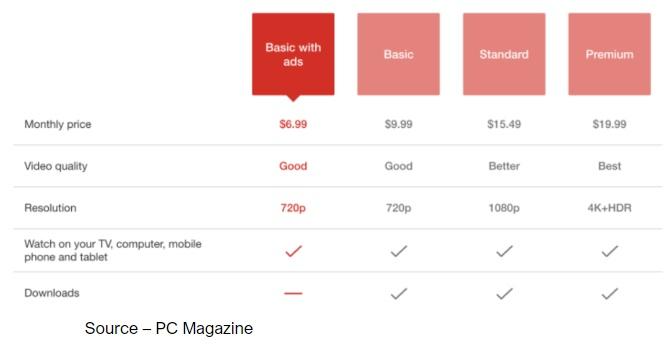

“Take Netflix,” he continued. “The basic plan here in the US at $7 with a few ads looks very appealing to people but it comes with some limitations consumers might find they miss … video quality and some limitations on new shows/movies that are ‘reserved’ for the higher priced plans.”

Give to Get – Consumers who are struggling to manage their entertainment budget often don’t weigh what they get and what they’re giving up to take advantage of a lower subscription fee. The industry will have to see if they change their minds.

“Some people will notice the video quality and resolution difference and will find they’re limited to the number of new movies and shows that are released and will make budget adjustments in other areas,” he continued.

“The same is true with all of the services adding an ad-supported tier,” he added. “The difference is that consumers now get to decide what they must have, what’s good to have and what’s right for them. So, it puts them back in control of their entertainment budget, which is important.”

The tiered offerings are also a sign that the industry is maturing as the major services turn their attention to future, long-term revenue growth.

Sandaros also made a couple of other big announcements that had NAB attendees cussing/discussing.

Amazon Prime and Apple TV+ have been working to play nice with the theater folks by saying they would be adding theatrical windows for major films enabling movie houses to realize more profit by putting more seats in their seats (and making it easier for them to be considered for statues).

However, Sandaros made it clear during the company’s quarterly report that Netflix would focus on being the best streaming service for consumers by offering the best range of entertainment variety – genres, national/international, live events, games – and offer password borrowers economic viewing options.

He surprised a lot of NAB attendees by saying, “Driving folks to the theater is just not our business.”

We probably would have sidestepped that statement, but we’ll have to see if he changes his mind later.

After all, once upon a time, they were never going to have ads on their service either.

Envelope Demise – The movie disc tucked and shipped in Netflix’s familiar red envelope says it all … the disc rental service is closing its doors so the company can focus all of its attention on global streaming growth.

But the move that no one saw coming was the fact that they were shutting down their 25-year-old red envelope business.

Except for one store in Bend, OR; Blockbuster disappeared from neighborhoods across the country — and others faded around the globe. The Red Envelope was the one vestige of “new movies” for us in the old days. It’s still important for people who don’t have reliable broadband service (about 6 percent of the population, 19M people).

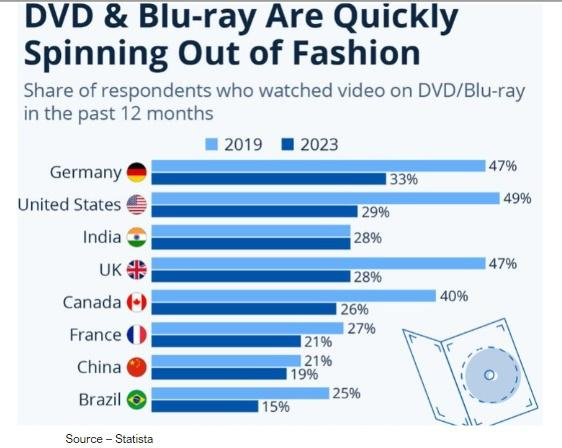

Spinning Down – DVD movie/show sales and rentals have enjoyed a long, healthy run and was what Netflix used starting in 1998 to launch its streaming service in 2007. Immediate online movie/show viewing is slowly – slower than you think – replacing disc sales/rentals as well as Pay TV.

We get it, global DVD sales have dropped significantly this past year and the trends aren’t good, but the announcement had a lot of NAB attendees asking WTF.

DVD rentals still accounted for more than $32M in revenue (5.2B discs) during the first quarter for the company, which would be a nice addition to most companies’ bottom line (Redbox owner Chicken Soup for the Soul, was asked with no reply).

We get Netflix not wanting to sell because the business really is a gold mine of customer data which they probably hope to mine for new streaming subscribers – even if it’s only AVOD – but still $30M + is $30M+ and probably pretty steady.

Still, the business already had a separate name – DVD.com – so why not simply spin it off as a privately held subsidiary that specializes in serving elitists who want to watch Blu-ray films and folks who don’t have/don’t want internet to their home?

Now we know why the postal service just announced a rate increase.

And since people change their habits less frequently than you might think, DVD viewing should continue to be a viable alternative to home viewing for at least 10 plus years.

Heck, we still buy CDs and records!

But, despite our questioning their kneejerk move, all of the streaming services are focused on steady growth compared to yesterday’s technology opportunities.

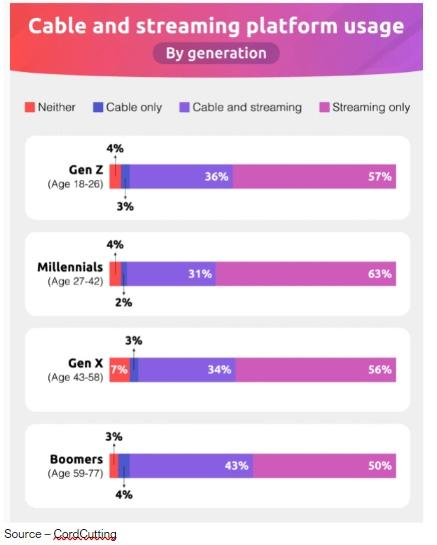

Direct Viewing – While traditional TV continues to grow slowly – very inexpensive – subscription and ad-supported streaming to screens of all types continues to become increasingly popular, especially with the Gen Z and Millennial crowds.

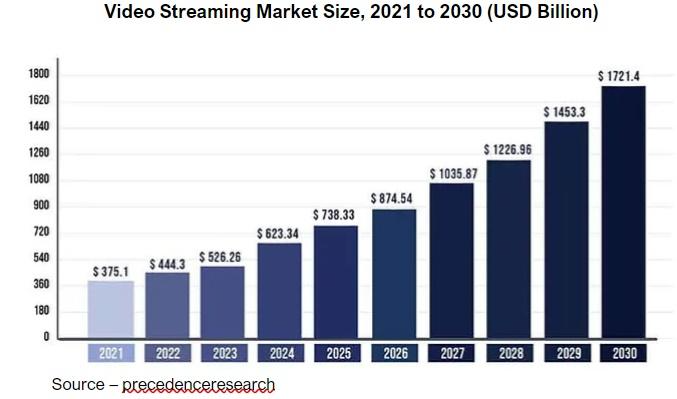

Global streaming should reach $156B by the end of this year and $217B by 2028 with more than 8B users, a user penetration of over 10 percent compared to 7.5 plus percent this year.

To get there, NAB members/exhibitors still have a hefty delivery list to improve video quality and streamline/assist content delivery.

MESA members and other providers are introducing new technologies that will enable higher-resolution video without increasing bandwidth or sacrificing speed.

New codecs that are being rolled out like H.266VVC and AV1 will cut bitrates in half, which will pave the way for making 4K and 8K resolution possible.

Several organizations introduced buffering resolution solutions at the show such as Fastplay and PlayAssure which will improve performance in slower internet situations and even improve 5G performance by reducing startup delays, rebuffering and other streaming quality issues.

But we believe one of the biggest opportunities/challenges – profitable ad-supported services – may be out of the streaming industry’s control.

The nearly 200 ad and FAST services reportedly hit $4B last year and will theoretically triple in five years.

Upfronts – The TV, streaming, social and news upfronts are a lot like movie trailers. Folks go to almost no end to show advertisers/agencies that you’d be crazy not to commit all of your marketing budget with them. And like trailers, that may be the best of what they have to offer.

Gawd, that sounds great but all of the services including YouTube, Instagram, Facebook, TikTok and others will be vying for those same ad dollars at next month’s ad and news upfronts.

And don’t overlook the proven ad service…traditional broadcasters.

Why should it be so tough?

Marketers and agencies are really comfortable with measuring their ad success because the half to one-hour show they advertise in racks up 5-10M viewers, obviously the show and ads are reaching and influencing a lot of the available market.

Social media is getting its cut of the ad budget because it’s reaching 10-100,000 people, even though the content around them is increasingly volatile, questionable.

But when it comes to streaming services, they measure minutes of viewing; and well, no one knows if their spot was in those minutes or not.

Forget the fact that the streaming service can give you tremendous insights into the individual viewers habits, likes, dislikes and more so you can tailor an ad for optimum reach/performance; it’s too difficult for creatives right now to think about/envision what’s right for the individual ideal customer.

Instead, it’s easier to create something for their boss and them.

We all know what Roger Sharp in Pinball: The Man Who Saved the Game, said is true, “Life is defined by risk; those you take and those you don’t. The ball is gonna drain no matter what, so find what you want and take a shot.”

But taking the shot and perfecting your game and the results takes time … lots of time.

The same is true in learning how to optimize the experience for the consumer and advertiser.

Maybe by the next NAB we’ll all up our game!

Andy Marken – andy@markencom.com – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media and industry analysts/consultants.