Entertainment is More than Movies, Shows

Content Insider #954 – Non-TV

By Andy Marken – andy@markencom.com

“You wanna play it soft? We’ll play it soft. You wanna play it hard. Let’s play it hard.” – Korben Dallas, “The Fifth Element,” Pinewood Studios, 1997.

The gal/guy who came up with the streaming marketing pitch – “watch any show/movie you want, when you want” – obviously didn’t have any young folks at home.

We wanted to watch a great movie last week that had just been released but the daughter wanted to watch this great live concert of one of her faves … she pouted, we lost.

Recently, we thought we’d try again but our son was already an hour into some stupid streaming video game (our description) and without taking his eyes off the set he said, “Just getting to the good part won’t be long, an hour or two”… thanks kid.

We’ve had to resort to streaming’s third pitch …” any screen.”

You know, home office computer monitor or staring at our smartphone screen for an hour or so.

Nope … no more!

Went to the big box store for another big OLED 4K HDR screen and sweet immersive surround sound set up.

Yeah, it’s necessary because tech folks took aggressive control of the entertainment content industry and are totally redefining, reshaping it.

The heck of it is the Gen Alpha/Gen Z folks fully embraced the change.

The people at Netflix, Amazon, Apple, YouTube and most recently Paramount are all hellbent on envisioning entertainment in its broadest terms with a strong dose of technology.

Yes, they’re in the business of creating/distributing long-form video stories in every genre possible; but that stuff is just a sliver of the total entertainment market they want to win.

Movies and shows range from attracting a few million folks to couch potatoes for a few hours, which are good but they’re expensive and have a limited shelf life.

Then they have to make or buy more to keep subscribers, convince some to come back and attract folks from other streamers.

The old ways aren’t working.

Just look at the movie industry.

Crowd Pleasers – Movie theaters no longer hold the mystic they used to because a movie is a movie no matter where people watch them and fewer people like to share the experience with 20-100 perfect strangers in a dark room while some are doing who knows what.

The movie/theater business struggled to reach $34.1B (about 500M tickets) this year, thanks largely to the release of a number of major franchise projects, heavy marketing and an increase in ticket costs.

Attendance is well below pre-pandemic levels which has been decreasing since 2002 when more than 1.5B people put their seats in theater seats.

Theaters won’t die but the idea of attendance revival with an exclusive long theater window? … that train left the station.

At the same time, the normal day/time TV has also shrunk down to its “hard core” audience and has … adjusted.

Convenient Entertainment – Streaming has become popular around the globe and continues to grow as high-speed, high-capacity wireless becomes universally available and inexpensive.

In comparison, the global video streaming market (movies/shows) reached nearly $625B in 2025 with about 1.1B global subscribers and more than 60 percent of the consumption being on mobile devices.

It’s estimated that the global market will be 6.8B handheld screen users by 2030 thanks to the expansion of high-speed internet access, smartphone proliferation and the steady increase of worldwide original content.

The tech-based streamers recognize the theater as a solid marketing tool; however, they really want the movies to be in their service.

But even better is a set of shows/series from the broadcast TV era that keep folks coming back for more and spin-offs if they’re lucky.

The great thing that global streamers have discovered is that there are great storytellers and stories that travel across borders beautifully.

The new leaders don’t spend all of their time in the studio and they’re shifting the way content is created, distributed and consumed along with other opportunities to engage the viewer.

They looked around and watched what the up-and-coming audience liked to spend their time on and expanded the idea of entertainment.

They’re taking a broader definition of personal and family entertainment that includes games, live events and almost anything that can attract individuals and crowds to a screen.

You might call it entertainment creep.

The New Breed

Changemakers – Amazon and Netflix started the trend of making it fast and easy for an individual to watch his/her content of choice and they continue to expand their offerings everywhere on any screen.

Amazon kicked off digital delivery in 2006 by renting video content that could be downloaded with their Unbox. A year later, Netflix launched its streaming service, offering subscription access to thousands of films.

They’re two different approaches but hey, video entertainment to the home is video entertainment to the home.

Amazon abandoned the download rental business, switched to Netflix’ subscription business model, bought MGM for $8.5B and got their hands on a vast library of iconic films/shows.

Of course, Amazon has always been more than a video service.

Heck, they sell/give folks access to almost anything they can make money on – video games, podcasts, books and more.

Both Netflix and Amazon keep expanding their content libraries, including adding their own original content to the mix as well as sports and special events.

It’s all guided by capturing, analyzing and using viewer data to focus on the global audiences as well as local/regional interests.

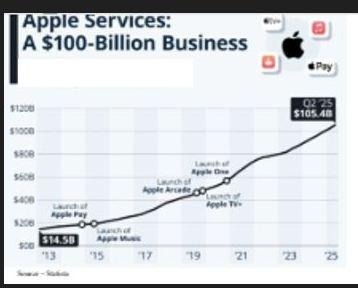

More Than Movies – Apple’s services are more than just great movies/shows, they also include content, materials that keep Apple users Apple users.

While Apple is mostly thought of as a hardware (Mac, iPhone) company with an installed base of more than 2.3B active devices, Apple services represent a business of about $100B a year.

Apple TV+ is most visible in the industry thanks to Oscar-winning films like Coda, The Boy, The Mole and other projects as well as widely acclaimed shows like Severance, Silo, Ted Lasso, For All Mankind and others.

At the same time, they’ve expanded their service offerings to include games, podcasts, music, edutainment and

Again, anything that would keep folks committed to their walled garden.

Big Bucket – YouTube started out as a personal video service and continues to derive most of its income from those sources but because of its massive user base, they are also adding content and services to “suddenly” have a significant entertainment presence.

It’s a helluva business … for Google/Alphabet.

Whether you’re a film person trying to get seen; an established actor who wants to stay connected with fans,

a filmmaker, a decision maker or just someone looking for her/his 3-5 minutes of fame; they’ll deliver the potential audience … more than 2.7B active users around the world who watch over 1B hours of video a day, 63 percent of the time on their smartphone.

Of course, they hype the heck out of their big traffic/moneymakers – creators – who can make $1 – $85M a year (if they really hump and are lucky).

But most make $1-$30 per 1K views or about $.018 per view, so it better be a side gig and an audience is … an audience.

Because they have such a huge audience, they’ve “expanded” their offerings by negotiating contracts to make

linear TV services available on their digital service and are expanding their offerings to include live events like

the NFL game that attracted about 17M viewers.

Undoubtedly, they’ll add more live events along with a modest investment in original shows/movies and other

stuff.

But it’s David Ellison’s Skydance that best exemplifies the new breed of home/personal entertainment that has everyone ducking for cover and focusing on their business.

It took patience, perseverance and laser focus to complete the acquisition of Paramount.

The company had been through some rough times, but Ellison wanted it because it had good bones – profitable linear TV channels, established and (begrudgingly) a respected news organization, a solid sports reputation, one helluva movie/show studio and an enviable content vault.

Ellison though isn’t satisfied with being a content creation/delivery player and certainly didn’t want to be defined as a nepo player.

He beefed up the company’s news organizations (CBS news) and 24/7 streaming news service; expanded the Paramount/Skydance sports organization with scripted/unscripted and live/studio programming, a new family.

f sports-focused interactive games/experiences and a team that could transform the company into a cutting-edge technology/entertainment influence.

But Ellison comes from a competitive family that doesn’t just want to win, it wants to dominate and change the landscape.

With the full support of his dad/family and even as the Paramount/Skydance organization was being finalized, he put a major bid on the table for WBD to create one of the biggest media companies in the US.

WBD has had a bloody history since David Zaslav took over as head man in 2002 along with a debt of $43B.

Yes, he reduced the debt by about $20B but it came at the cost of $5B non-content costs, shelving completed projects (tax write-off) and lots of people, strategic missteps, continual reorganization, branding/rebranding, corporate restructuring and shrinking revenues which might be why shareholders rejected his $52M compensation package.

Of course, WBD still has a $35B debt to deal with and a company that only has a market cap of $40B so the price might be right if the FCC can understand it’s in everyone’s best interest.

Ellison (David) understands the zero-sum approach to business he learned from his father, Larry Ellison, the richest man in the world ( as of this writing) who spent about $875M to win the Americas Cup (twice) and risked his life in the 1998 Sydney to Hobart Yacht Race that resulted in five sinkings, six sailors dying and also became known as the race’s deadliest disasters.

To prove the tree doesn’t fall very far from the Apple, the elder Ellison is probably eyeing the US portion of TikTok if/when it becomes available because it would be a nice fit with Oracle which he founded and has become one of the country’s leading cloud service companies.

Why else spend much time on the DC Beltway?

Shifting Habits

All of the tech-driven streaming firms clearly see that the viewing audience and habits are

shifting.

The global streamers see that people are attracted to niche and international shows/movies and

that today’s data-driven personalization helps them quickly and effectively recommend content

folks will want to watch – projects in a range of genre, news, sports and more.

At the same time, video games have evolved from a niche hobby into a dominant cultural and

economic force.

Ad it’s not just local or regional, it’s global.

Gamers pioneered interactive and immersive entertainment and Netflix has found that projects like Black Mirror: Bandersnatch can get subscribers involved and coming back for more.

Gaming IP like The Witcher and The Last of Us have shown they can attract and keep gamers involved as well as people who just like a good movie/show.

Competitive gaming (esports) draws millions of viewers.

With every Gen Alpha/Gen Z almost born with a smartphone in their hands, there’s a range of mobile games to fit almost everyone’s taste and interest; and when combined with in-game ads/purchases, it can be very profitable way to keep subscribers.

While Apple follows its “prestige” strategy, Netflix, YouTube and Amazon have tended to focus on the casual

and “new” gamer.

It’s Better Live

Shared Choices – With streaming, people everywhere are increasingly able to watch the sport of their choice no matter where the contest is being held. In addition, streaming has exposed folks to new sports that they add to their “gotta watch” lists.

O.K., let’s state the obvious. People like sports – futbol, Lacrosse, football, baseball, basketball, volleyball, table tennis, rugby, cricket, wrestling, boxing and car races, you get the idea – and a lot of these folks would like to be at the game/event.

But most enthusiasts end up watching it on their home/personal screen because it’s cheaper/almost as good and admit it, you have the best seat in the house.

Need to share the excitement with others … share the screen.

For years, sports were the exclusive realm of linear TV and a welcome source of large audiences and ad income.

But streamers perfected low-latency technologies that reduced delays of a few minutes to seconds and despite a few “learning” technical gaffs, they showed they were ready and anxious to play.

And they had the deep pockets sports, leagues, franchises and teams that were willing to work with.

Fubo (70 percent owned by Disney), ESPN+, Dazn, and now every major streaming service is signing up for as many different activities as possible that best match their subscribers’ viewing tastes.

Investing an estimated $417B in 2025, streaming is expected to account for about 25 percent of the global sports rights market.

More local, regional and global “opportunities” are being discussed. In addition, a lot of niche sports agreements like billiards, bowling, underwater hockey, Kabaddi, Quidditch and others are entering the arena while sports like Formula 1, NASCAR and cycling are building a stronger global following.

Almost As Good – Live concerts are a multi-billion-dollar business and streamers have found that showing them in realtime is almost as good for the audience as actually being there … almost. Best of all, they don’t churn mid concert. Live event streaming – concerts, standup comedy, plays, etc. is a “new,” rapidly growing sector that is projected to be worth hundreds of billions of dollars by 2030.

Taylor Swift and Beyonce set the stage on fire and showed that people (O.K., young folks) wanted to enjoy the experience of a concert/show, even if they weren’t able to see it in the middle of the audience.

Netflix tested the waters early with stand-up specials including Chris Rock, Lady Gaga, John Mulaney and a steady stream of shows.

The real-time “being there” entertainment is rapidly gaining momentum (and a following) thanks to the advanced use of technology to put you in the center of the excitement.

It’s true, industry awards events have experienced a decrease in viewership; but admit it, the thank you speeches are “a little” long/boring and well, they all seem pretty much the same with only a few “surprises” to spice up the evenings.

Subscribers, viewers and shippers are showing that they want their stuff, and they want it now and on their schedule.

Technology has changed the personal/home entertainment landscape as more people expand and refine the creator-to-fan direct model driving revenues for creatives and ultimately studios, IP holders, franchise owners and streamers.

Yes, the industry is shifting beneath our feet and even the well-established stalwarts are adjusting.

While Disney is preparing to anoint a replacement for finally retiring Bob Iger the company has retargeted it’s linear TV (ABC, ESPN) to adjust to the new environment and has begun leveraging its massive internal technology expertise and IP library to hang onto its total entertainment house title.

Now that Lachlan is now firmly in control of the Aussie, British, US media empire we’re already see the conservative organization make changes in its linear TV business and increase its presence in streaming news/entertainment/sports activities as well as strengthen it’s free-to-view Prime TV service.

Change may not come easy to them, but they also know that standing still isn’t an option.

Streaming hasn’t just redefined when, where, how we watch entertainment but it has opened up new opportunities for people young and old to zero in on exactly what they envision doing with their “spare” time when they want to relax or experience or learn something new, different or maybe just spend some time with something that’s familiar/comfortable.

Movies and shows are now just one of the entertainment choices people have and streaming services have to offer them to remain relevant.

They’re all interesting, they’re all important and they’re all entertaining … to the global viewer.

As Mondoshawan said in The Fifth Element, it’s your mission to pass your knowledge on to the next as it was passed on to you.

And as Zorg reminded us, “If you want something done, do it yourself. Yep!”

No one said it would be easy or honestly, even glamorous.

Andy Marken – andy@markencom.com – is an author of more than 900 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. He is an internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in the storage, storage management and film/video production fields. He also has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.