2024 Has a World of Potential for the Industry

Content Insider #837 – Reset

By Andy Marken – andy@markencom.com

“Without the burden of memories, we’re a clean slate, we can have a fresh start. Nobody can tell you who you are but you yourself. This world is created by our thoughts. The rules are different here.” – Yan, “Coma,” Big Sky Films, 2019

Don’t know how to tell you but this was not the year we looked forward to this time last year.

Yes, 2020 was close to being a complete disaster, but most of us made it through with bare bones sanity.

2021/22 was all about shaping things up, getting a handle on what the new normal was going to be and getting ready for a year that would knock our socks off.

This was the year that was going to rock!

Okay, the year wasn’t BAD but it was just bad enough to seismically change the course of most of the industry’s plans and goals.

So, let’s see what tomorrow has in store for us.

First, let us clarify our position at the outset … we like to make our own mistakes so, AI?

No freakin’ way!

After all, we’ve never seen an AI movie that ended well.

However, it’s here/coming, especially in the film/show industry.

It’s going to save time, money,and improve the product. Just ask the “experts.”

Everyone wants their piece of the action, even though few can describe it other than it’s going to be great.

Dive in … what could possibly go wrong?

No one really knows what’s under the surface.

Even techie leaders like Andrew Ng, Andrej Karpathy, Dennis Hassabis, Geoffrey Hinton, John McCarthy and others warn that we have to go slow, be cautious with it.

But it must be good and safe because people are throwing millions at it … and it’s going to be worth billions!

And they’ll be riding on golden chariots, when they get there.

If you thought crypto currencies were the pot of gold at the end of the rainbow, you ain’t seen nothin’ yet!

AI guardrails were certainly a major discussion point during the writers/actors negotiations/agreements. But also a distraction point too.

Writers/actors had a tough time with it because they thought it might curtail or limit their careers.

Studio bosses had a tough time with it because wholesale use of AI could help give them better control over the stuff they show and the profits they hoped to make.

We’ll see who negotiated best.

But…

AI tools have been used in film/show production for years; and in some areas, they’re getting better, more useful, more appreciated.

For example, for executives with the job of greenlighting projects, AI is the go-to tool.

Instead of relying on his/her seasoned opinion, AI data crunching/analysis will tell them what viewer acceptance/engagement will be before any time/effort has been invested.

It will help them select the best cast and crew based on their track record with the desired target demographics.

It will optimize all of the resources, making pre-production faster, easier and the results more predictable.

It will help source alternative and more cost-effective locations since SoCal is getting to be a ridiculously expensive place to shoot.

If the visual story doesn’t meet expectations, “Hey, it told me to do it!”

Post-production tools and solutions from Adobe, Avid and Da Vinci (Blackmagic) have been enthusiastically accepted by video/audio editors, VFX experts and workflow pros who have always been under ridiculous budget (time/money) restraints.

Sometimes the final product exceeds everyone’s expectations, including viewers.

Stress Test – Whether it’s on the big screen, the screen at home or the screen in your hand, the only real measure of a project is how it resonates with the target audience. Sometimes it’s just a gut-feeling and that’s hard to quantify.

Then they don’t, remember what greenlighted the project.

Whether your video story is destined for theaters, homes or both; no film or show will appeal to all 8B+ individuals on the planet no matter what you (and the technology) do.

Studios/streamers/networks and writers/actors all agree that tools that can help influence diehard, casual and occasional viewers to visit their preferred screen and watch films/shows are good for everyone.

Technology-based folks like Netflix, Amazon and Apple have honed and refined their personalized marketing tools to increase ticket sales/stream attention/views.

The data-based tools identify optimum release dates, marketing messages and message channels.

Anything that can improve ROI for production and streaming companies has their – and shareholder – support.

But … that’s where we philosophically draw the line.

AI writing a script?

AI-generated images of folks in the project?

Sure, people can do it … and will.

However, what do we sacrifice in the process?

Writing is hard.

Great writing is damn hard!

And that’s what gives people such satisfaction in finishing a project.

Back in 400-something BC, Plato is quoted as saying writing is the geometry of the soul.

It empowers, inspires, nourishes the writer(s) and the audience.

Ones and zeros can never do that.

By the same token, we can copy, duplicate and animate the visual aspects of a person for a scene or segment of a film/show but what do we lose? The AI-generated “presence” has no ability to think or feel, has no soul or feeling of self-worth.

And it has no humanity to enable people to connect with others in order to like, hate, empathize, feel.

That matters.

Otherwise, it’s like one hand clapping … just moving air around.

However, now that writers and actors are back in their writing rooms and on sets, studios and streamers are focused on tomorrow.

They all need to recover the $6B plus lost during the strikes and make up for lost time.

Streamers/studios need to expand and produce profits from their D2C service … with a side order of theatrical releases.

It’s especially true for Disney which is wrapping up its nearly $9B deal with Comcast to take over the final one-third of Hulu.

At the same time, it’s working on unloading its stake in the India-based properties — Reliance, Hotstar and Star India — for about $10B.

As for the real value of their legacy, ESPN and streaming ESPN+ is as fuzzy as the entire sports marketing arena.

Leagues, franchises and teams – professional, college, high school – are looking to increase their asset value and revenue stream (greed).

It can only make it more difficult for sports enthusiasts to find a go-to sports service.

But back to tomorrow’s screen viewer.

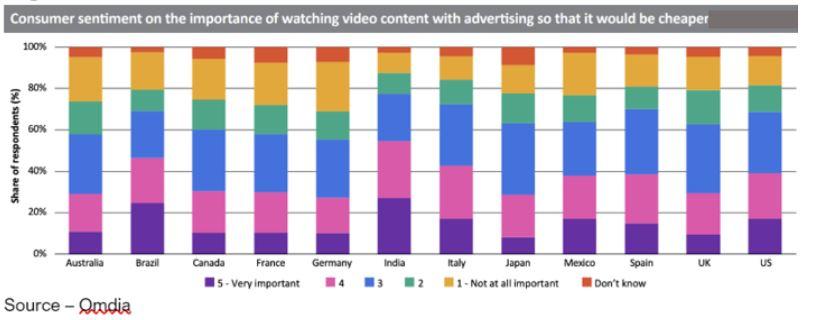

Money Talks – Researchers like to tell us that people hate ads interrupting their content; but when it comes to really paying for their entertainment, they’ll take the ad-supported stuff almost every time.

Who would have thought that people were actually interested in saving a few bucks, pesos, euros, whatever while enjoying their content on whatever screen along with a side order of a few ads.

This is where growth is predicted to happen in 2024 and for a few years beyond.

To get away from raw subscriber fluctuation and focus on what really matters – ARPU (average revenue per user), SVOD services are abandoning the idea of death by a thousand paper cuts.

They’ll continue increasing their monthly fees to a point where if you want to avoid ads it’s going to cost … a little more.

In addition, they’re shifting to tiered pricing plans – SVOD (ad-free), AVOD (lower-cost ad-upported) or licensing some of their content to FAST (free with ads) services to give folks options.

Whether it’s an ad-supported or FAST, the services want to profitably get their content to as many viewers as possible.

More importantly, they want to use AI to leverage viewer data as efficiently and effectively as possible to really understand what people want to watch and what commercial slots to sell to marketers.

Migration – Ad dollars will follow consumers in the years ahead, especially since marketers will be able to more efficiently and more effectively reach specific prospects rather than irritating the entire crowd.

In their October earnings report, Netflix surprised the rest of the industry – and Wall Street – by proving you can clamp down on password sharing and the world won’t come to an end.

They reported that their year-old ad tier had already grown to 15M global users; and it will continue to grow, thanks to their global relationships and AI tools that enable them to pick film/show winners.

Granted, they haven’t convinced all of their subscribers to knock it off, but they no longer have the dubious crown of having more freeloaders than everyone else.

Well, Okay – Other streaming services and Wall Street snickered when Netflix announced it was clamping down on password sharing but they only proved that given economic options viewers would stay. Expect others to follow suit nest year.

After Disney gets through reworking their asset portfolio, they will focus on “encouraging” more folks to take advantage of their two ad-supported offerings – Disney + and Hulu – and improve their ARPU.

Paramount has spent a lot of time and effort realigning and restructuring its organization during the content lull, including beefing up their ad backend for marketers.

Expect to see them pay more attention to ARPU for both Paramount + and Showtime rather than striving for subscribers at all costs.

Still, weak content is weak content no matter how viewers pay for it, so they have to make a tough call – invest in great creative work or simply license shows/films and ride their Paramount pay TV channel as long as possible.

Unfortunately, Apple’s upcoming ad tier won’t affect our household entertainment budget.

Our daughter is one of the loyalists who prefers the Apple One bundle – Apple TV+, Apple Arcade, Apple Music, etc. – so we’re stuck.

But marketers will find it attractive because Apple has had a great track record. With their show/movie selection and subscriber base of 1B folks globally, it is tantalizing to say the least.

FAST is becoming even more interesting to viewers and marketers since the ad load is lighter (15-20

m/h for yesterday’s payTV compared to streaming’s 4-10 m/h).

Going Global – FAST channels in the Americas are becoming increasingly inviting to viewers and marketers as they improve their infrastructure and content offerings. The big move in the coming year will be to expand globally.

Currently, the US accounts for 90 percent of the FAST market.

Studios, including Disney, WBD and Paramount are licensing more original and library projects to make them more attractive than just offering a pile of old stuff.

FAST providers will finally develop better ways of helping viewers find content they want to watch (AI-enabled selection suggestions) and standardize viewer information to make the services easier to use and more valuable to advertisers.

In addition, they’ll refine tools that will allow marketers to pick specific marketing profiles, so ads are less intrusive and more effective.

Expect them to deliver more creative advertising opportunities, including product placement and specific genre selection.

Best of all, FAST will finally move beyond their English-only home court and begin to become global service providers.

Allan McLennan, president of 2G Digital Post, said ad-supported and FAST services are reshaping the entertainment option picture with seamless viewing across a variety of original and exclusive content offerings.

“Expanding globally is still in its infancy,” McLennan emphasized, “But demand for multinational viewing options here in the Americas is becoming a major viewing consideration. We’re seeing services like the FAST powerhouse PlutoTV expanding their growth, including a UK partnership with the television network My5 to extend their reach with language-specific channels and deliver content to underserved cultures.”

Localizing – FAST services like Pluto will increasingly use AI to deliver content to viewers in their native tongue whether it’s by adding subtitles or dubbing tapping the support of global and regional AI-enabled localization services.

While English is the leading language in the US (25M), nine other languages (Spanish, Chinese, Tagalog, Vietnamese, Arabic, French, Korean, Russian and Portuguese) are spoken by people who have integrated without assimilating into the US culture.

“Airing content in their native language produces a dedicated audience that appreciates that the service respects their culture,” McLennan emphasized, “and everyone wins.

“At the same time,” he continued, “the services are increasing their international growth in Europe, the Middle East and SEA (Southeast Asia)/Oceania by localizing content for cross-border viewing as well as reverse migrating into the US to connect with their expats.”

He noted that localizing content with subtitles or by dubbing would have been cost/time prohibitive without AI-enabled processes.

Global organizations like 2G Digital Post in Burbank, California provide economic, reliable and intelligent media optimization and localization support for the studios, broadcasters and streaming services.

“It simply wouldn’t have been possible a few years ago, but with now applicable generative AI solutions we are starting to see an increase in the AI learning and a bit better accuracy,” McLennan added.

Ad Growth – FAST and ad-supported services will continue to show solid growth in the coming years as people become more accustomed to reading subtitles while watching a show/film or enjoy perfectly AI-dubbed content. Marketers will also benefit with better, more effective ads that are also no longer abrasive/intrusive.

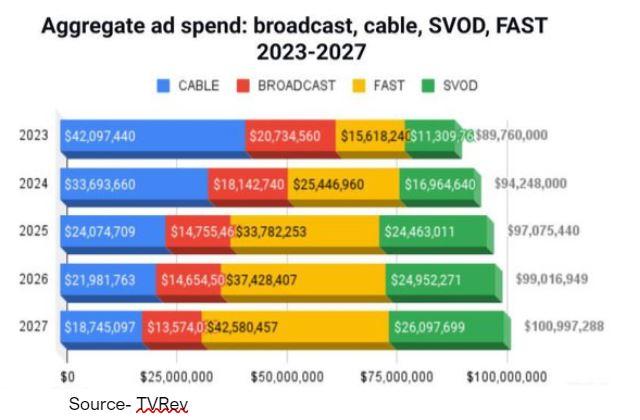

The new local and international approach will play a key role in ad-supported/FAST services topping nearly $27B this year and rising to more than $68.5B by 2027.

Just for clarification, TVREV classifies subscription-based streaming services with ad-tiers as SVOD.

But the real point is ad-supported streaming will grow because:

- People are willing to reduce their entertainment financial budget in exchange for a few, well-developed and targeted ads

- Services will ensure they grow their subscriber base with reasonable or no subscription fees while providing advertisers with a greater understanding of the viewers

- Marketers will more intelligently and creatively produce and place ads that are tailored to the viewer so he/she/they are more receptive to the advertising message

- Buying and measurement standards will emerge that will help all parties understand the importance, value and propriety of the first-party data.

2024 will be a year that is hell-bent on developing, finalizing and launching new shows/films.

This year, the US industry released 43 compared to 179 in 2019 and it’s time for the industry to learn and adjust in real time.

Yes, there are new guidelines.

Yes, there are new tools.

Yes, there are now opportunities.

Now it’s up to the people involved to make the best decisions to reshape the landscape for tomorrow’s industry.

As Yan said in Coma, “What if we started from scratch, no memories. What if we designed an island that was

never seen before. A place that wasn’t attached to any memories. That would make us safe.”

It sounds like a great way to move the entertainment industry forward … for everyone.

We certainly can’t afford another relapse!

Andy Marken – andy@markencom.com – is an author of more than 800 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.