Spotify Technology S.A. Announces Financial Results for Third Quarter 2019

NEW YORK–(BUSINESS WIRE)–Spotify Technology S.A. (NYSE:SPOT) today reported financial results for the third fiscal quarter of 2019 ending September 30, 2019.

![]()

Dear Shareholders,

The business met or exceeded our expectations in 3Q19, with accelerating MAU growth, and better than expected (1) Subscriber growth, (2) Gross Margins, and (3) Operating Profit. For the 8th consecutive quarter, free cash flow was positive. We continue to see exponential growth in podcast hours streamed (up approximately 39% Q/Q) and early indications that podcast engagement is driving a virtuous cycle of increased overall engagement and significantly increased conversion of free to paid users. The correlations in our data sets are clearly apparent. We are working to prove causality. Overall, the business is performing strongly.

CFO TRANSITION

After playing a pivotal role in Spotify’s listing and helping to establish Spotify as a public company, Barry McCarthy will retire from Spotify on January 15, 2020, stepping down as the company’s CFO. Barry will be replaced by Paul Vogel, who is currently Spotify’s VP of FP&A, Treasury and Investor Relations. Paul and Barry have worked together closely for the last 3 years. Pending shareholder approval, it is expected that Barry will be re-appointed to the Spotify Board of Directors, a role he held prior to joining the company as CFO.

MONTHLY ACTIVE USERS (“MAUs”)

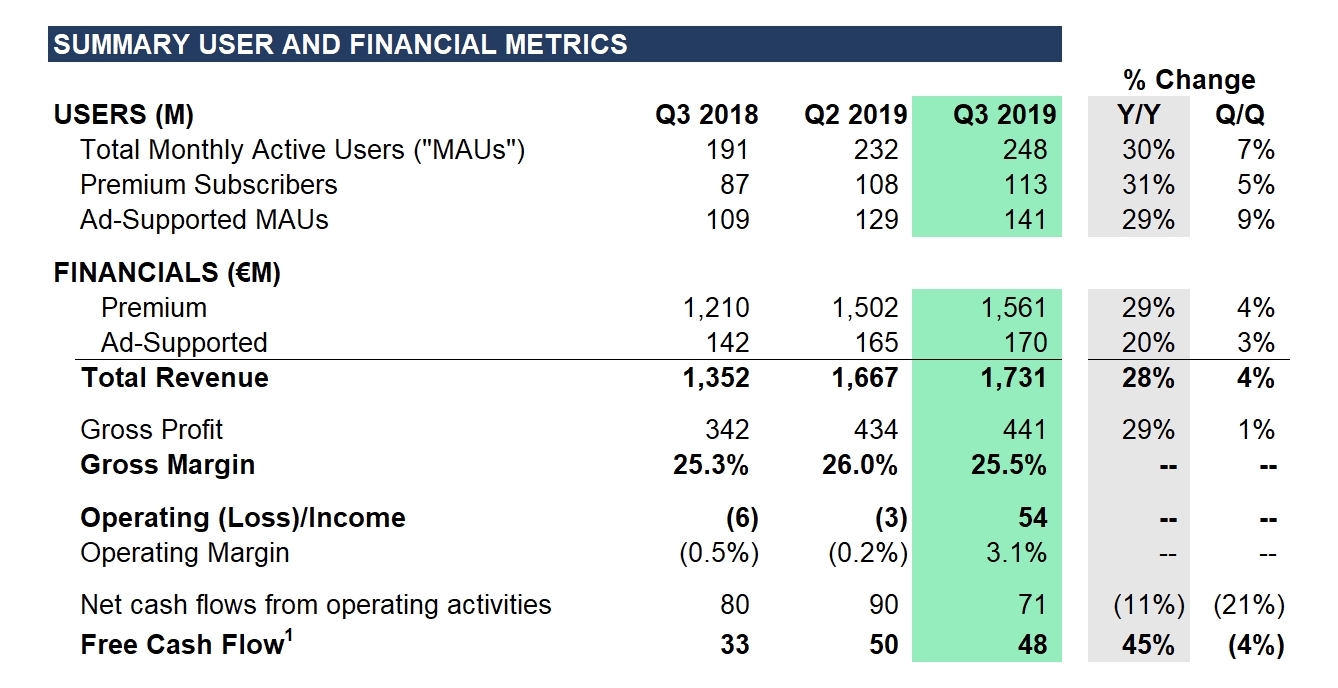

Total MAUs grew 30% Y/Y to 248 million, outperforming the high end of our guidance.

Developing regions continue to be a significant driver of this outperformance. Growth in Latin America accelerated sequentially for the 2nd consecutive quarter as retention among newer users continues to improve. Southeast Asia remains our fastest growing region (excluding India), and Y/Y growth in Q3 accelerated 1400 bps vs. 3Q18. Of note, India outperformed our forecast by 30% this quarter. This momentum was driven by a number of factors including the launch of our first broad-based marketing campaign, “Sunte Ja” (“Listen On”), since launch in February.

As we discussed last quarter, a portion of the faster MAU growth is a result of our continued product innovation driving improvements in long-term retention. We rolled out a number of tests in Q3 with the goal of immersing new users in the product functionality faster. It’s still early, but we are encouraged by the improvements we’ve seen in retention to date. Our belief is that a better onboarding experience leads to increased engagement, which leads to better retention, conversion, satisfaction, and ultimately, lifetime value. Expect us to continue to innovate like this in the future.

PREMIUM SUBSCRIBERS

We finished Q3 with 113 million Premium Subscribers globally, up 31% Y/Y. Net Subscriber growth exceeded our expectations and was led by strong performance in both Family Plan and Student Plan. All other product offerings were mostly in line with expectations.

Within Family Plan we launched a slate of product upgrades, the first meaningful changes in some time. Subscribers now have access to new features designed specifically for families including parental controls to filter explicit content, a Family Mix playlist with personalized songs for the whole family, and a family hub where master account holders can easily manage all settings in one place.

Early September saw the expansion of our Duo pilot from the original 5 pilot markets into an additional 14 markets including most of Latin America. Additionally, we kicked off our annual “back-to-school” promotion of the Student Plan, a campaign that ran across 17 markets including the U.S. and parts of Europe. Finally, we announced a U.S. partnership with AT&T, which offers Spotify Premium as an add-on to select wireless plans, and offers a 6-month free trial to certain eligible bundle subscribers

In August, we launched a test of a new 90-day free trial offering to Standard and Student Plans. Family Plan was added in October. The test performed in line with plan and was not the reason Subscribers outperformed guidance in the quarter. We believe the 90-day offering will have positive benefit to growth and retention moving forward.

Churn improved 19 bps Y/Y and 7 bps sequentially.

Competition

We continue to feel very good about our competitive position in the market. Relative to Apple, the publicly available data shows that we are adding roughly twice as many subscribers per month as they are. Additionally, we believe that our monthly engagement is roughly 2x as high and our churn is at half the rate. Elsewhere, our estimates imply that we continue to add more users on an absolute basis than Amazon. Our data also suggests that Amazon’s user base skews significantly more to ‘Ad-Supported’ than ‘Premium’, and that average engagement on our platform is approximately 3x.

FINANCIAL METRICS

Revenue

Total revenue of €1,731 million grew 28% Y/Y in Q3. Consolidated revenue modestly beat our expectations with Premium outperforming and Ad-Supported weaker than forecast. Premium revenue was €1,561 million, up 29% Y/Y, while Ad-Supported revenue was €170 million, up 20% Y/Y.

For the Premium business, average revenue per user (“ARPU”) of €4.67 in Q3 was down 1% Y/Y (down 3% excluding the impact from FX rates). The largest driver of ARPU decline continues to be product mix, although geographic mix also plays a role. As a reminder, approximately 75% of the impact to ARPU is attributable to product mix changes, and the remainder a function of changes in geographic mix and other factors.

For the Ad-Supported business, revenue growth of 20% Y/Y underperformed our expectations in Q3. Roughly 80% of the miss was related to self-inflicted implementation and integration issues we experienced with the rollout of a new order management software to replace Google’s Doubleclick Sales Manager which was sunset in July. This resulted in a combination of lost orders and under delivery of other orders totaling about €9 million of “lost” revenue. The balance of the revenue shortfall related to a slowdown in programmatic growth from 65% Y/Y in Q2 to 48% in Q3, mostly related to a slowdown in video PMP revenue. Programmatic revenue was sluggish early in the quarter but regained momentum during Q3. Podcasting revenue outperformed expectations with strong Y/Y growth but is still a relatively small slice of the total Ad-Supported business at less than 10% of total ad revenues.

Gross Margin

Gross Margin was 25.5% in Q3, 30 bps above the high end of our guidance of 23.2-25.2%. The largest contributor to outperformance stemmed from our core music gross margin. Royalty costs were more favorable than expected due to product and revenue mix. We also had lower content expense resulting from both lower overall spend and the slower rollout of developed shows. Similar to the trends we saw develop in Q2, Q3 saw continued efficiencies in streaming delivery and payment expense.

Premium Gross Margin was 26.5% in Q3, down seasonally from 27.2% in Q2 and up 40 bps Y/Y. Ad-Supported Gross Margin was 16.0% in Q3, up from 15.8% in Q2 but down 260 bps Y/Y.

Operating Expenses / Income (Loss)

Operating expenses of €387 million in Q3 increased 11% Y/Y, significantly less than the pace of revenue growth. Operating Profit was €54 million, an Operating Margin of 3.1%. Share price performance and the associated social charges were a significant driver of this outperformance versus expectations, but we would have been profitable even without this impact. Other drivers of our better than expected profit in the quarter were higher Gross Profit and lower than expected spend across artist marketing, promotion of original content, R&D, and G&A.

The decline in our share price in Q3 decreased operating expenses more than plan because of reduced social charges on stock-based compensation. The decreased social expense contributed approximately 160 basis points to our Operating Margin. As a reminder, these costs are payroll taxes associated with stock based compensation. We are subject to social taxes in several countries in which we operate, although Sweden accounts for the bulk of the social costs. We don’t forecast stock price changes in our guidance so upward or downward movements will impact our reported operating expenses.

Podcasts

We continue to see exponential growth in podcast hours streamed (39% Q/Q for 3Q19), albeit off of a small base. Podcast adoption has reached almost 14% of total MAUs. The U.S. accounts for the largest share of podcast streams but share of listening is higher and growing faster in several European countries. Podcast engagement is clearly a growing global phenomenon.

For music listeners who do engage in podcasts, we are seeing increased engagement and increased conversion from Ad-Supported to Premium. Some of the increases are extraordinary, almost too good to be true. We’re working to clean up the data to prove causality, not just correlation. Still, our intuition is the data is more right than wrong, and that we’re onto something special. So expect us to lean into our early success with podcasting and to share more insights with you when we’ve established causality.

We continue to ship updates to our podcast experience, and now have more than 500,000 podcast titles available on the platform. Q3 saw the launch of 22 original and several other exclusive titles from Spotify Studios such as The Ringer: The Hottest Take and The Conversation with Amanda de Cadenet in the U.S. We also announced the release of a number of Gimlet and Parcast originals, including Gimlet’s The Clearing and The Journal, as well as Natural Disasters, Medical Mysteries, and the Summer of ‘69 from Parcast Studios. We are continuously working to expand our global podcast library with the introduction of El Primer Café in Colombia, and London, Actually in the UK.

Two-Sided Marketplace

At our Investor Day presentation in March 2018 we said the goal of our marketplace strategy is to harness Spotify’s ability to drive discovery to connect artists with fans on a scale that has never before existed with the goal of enabling 1 million artists to live off of their work.

The strategy has been about going from a one-size fits all model to a model that better fits the various types of content and creators on our platform. Through a combination of tools, services, and programs we will be able to serve creators better and build a better business for Spotify by leveraging our demand creation capabilities. So Marketplace is about meeting the needs of creator teams to create art, engage with, grow, and better monetize their fanbase.

These initiatives drive both revenue growth and content cost savings. We expect to give more detail on the financial benefits of the Marketplace and the impact on 2020 guidance on the 4Q19 earnings report.

Recent highlights of positive developments with our marketplace strategy include:

- Spotify for Artists – Valuable analytics, identity management, and promotion tools with more than 465,000 monthly active artists, up 365% from the 100,000 announced at Investor Day. These monthly active artists account for ~80% of the streams on Spotify. Key recent additions to the feature suite is Canvas – a tool that enables artist teams to add looping visuals to their tracks. Many artists have seen substantial uplift in their streams by using this tool.

- Sponsored Recommendations – Available to select major and independent label partners as part of our recently announced paid beta in the U.S., this is Spotify’s first cost per click ad product which leverages our listener graph of music tastes to promote new releases to free and paying users.

- SoundBetter – In September, we announced the acquisition of SoundBetter, a music production marketplace for artists, producers, and musicians with 180,000 registered users.

Lease Accounting

Starting January 1, 2019, we adopted the new lease accounting standards dictated by IFRS 16. This required certain leases which were accounted for as operating leases be treated as finance leases going forward. Certain leases were reclassified as assets and liabilities on the balance sheet which yielded increased depreciation and interest expense, offset by a reduction in rental expense. We recognized €9 million of lease liability interest expense in finance costs during the third quarter of 2019.

Free Cash Flow

We generated €71 million in net cash flows from operating activities and €48 million in Free Cash Flow in Q3. We maintain positive working capital dynamics, and our goal is to sustain and grow Free Cash Flow, excluding the impact of capital expenditures associated with the build-out of new and existing offices. We paid out approximately €26 million associated with our office builds in Q3. We expect to complete office build-out projects in Stockholm, São Paulo, and Boston in Q4 2019. We expect to complete the remaining projects over the next four quarters at a cost of roughly €165 million.

We ended Q3 with €1.6 billion in cash and cash equivalents, restricted cash, and short term investments.

Share Repurchase Program Update

On November 5, 2018, Spotify announced a program to repurchase up to $1.0 billion of its publicly traded shares. During Q3, the Company repurchased 1,130,675 shares at a total cost of $142.1 million and an average cost of $125.68 per share. Through September 30, the Company has repurchased 4,210,251 shares at a total cost of $554.5 million and an average cost of $131.71 per share. This total cost is approximately equal to the $552 million in cumulative Free Cash Flow generated by Spotify since the start of 2018.

Q4 2019 OUTLOOK

These forward-looking statements reflect Spotify’s expectations as of October 28, 2019 and are subject to substantial uncertainty. We are reiterating our previous ranges with the exception of Total MAU, which we are adjusting higher due to continued outperformance.

Q4 2019 Guidance:

- Total MAUs: 255-270 million

- Total Premium Subscribers: 120-125 million

- Total Revenue: €1.74-€1.94 billion

- Gross Margin: 23.7-25.7%

- Operating Profit/Loss: €(31)-€(131) million

Given the performance of Spotify’s stock over the last twelve months, let’s consider today’s guidance from a slightly broader perspective. Look back to March 2018 before our direct listing. Compare the Street’s expectations then for FY 2019 to our guidance now. The 12 month target stock price then was $181 and the consensus forecast (the average forecast of the 18 equity research analysts who covered us prior to 1Q18 earnings) for 2019 was actually lower than today’s guidance for this year’s results. The business is outperforming and the stock price is down 33% vs. the consensus. Sometimes the stock price reflects the performance of the business and sometimes it doesn’t. But eventually, it always does.

|

|

Street Consensus[2] |

Spotify Guidance |

|

MAU[3] (M) |

256 |

266 |

|

Subscribers (M) |

122 |

123 |

|

Revenue (€M) |

6,610 |

6,755 |

|

Gross Margin |

25.9% |

25.1% |

|

Operating Loss (€M) |

(195) |

(133) |

|

Stock price (target/actual) |

$181 |

NA |

Note: Spotify guidance based on actuals for Q3 YTD + 70th percentile of guidance for 4Q19

EARNINGS QUESTION & ANSWER SESSION

The Company will host a live question and answer session starting at 8 a.m. ET today on investors.spotify.com. Daniel Ek, our Founder and CEO, and Barry McCarthy, our Chief Financial Officer, will be on hand to answer questions submitted to ir@spotify.com and via the live chat window available through the webcast. Participants also may join using the listen-only conference line:

Participant Toll Free Dial-In Number: (844) 343-9039

Participant International Dial-In Number: (647) 689-5130

Conference ID: 4774562

Use of Non-IFRS Measures

To supplement our interim condensed consolidated financial statements, which are prepared and presented in accordance with IFRS, we use the following non-IFRS financial measures: Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect, Ad-Supported revenue excluding foreign exchange effect, EBITDA, and Free Cash Flow. Management believes that Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect and Ad-Supported revenue excluding foreign exchange effect are important metrics because they present measures that facilitate comparison to our historical performance. However, Revenue excluding foreign exchange effect, Premium revenue excluding foreign exchange effect and Ad-Supported revenue excluding foreign exchange effect should be considered in addition to, not as a substitute for or superior to, Revenue, Premium revenue, Ad-Supported revenue or other financial measures prepared in accordance with IFRS. Management believes that EBITDA and Free Cash Flow are important metrics because they present measures that approximate the amount of cash generated that is available to repay debt obligations, to make investments, and for certain other activities that exclude certain infrequently occurring and/or non-cash items. However, these measures should be considered in addition to, not as a substitute for or superior to, net income, operating income, or other financial measures prepared in accordance with IFRS. For more information on these non-IFRS financial measures, please see “Reconciliation of IFRS to Non-IFRS Results” table.

Forward Looking Statements

This shareholder letter contains estimates and forward-looking statements. All statements other than statements of historical fact are forward-looking statements. The words “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible,” and similar words are intended to identify estimates and forward-looking statements.

Our estimates and forward-looking statements are mainly based on our current expectations and estimates of future events and trends, which affect or may affect our businesses and operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to numerous risks and uncertainties and are made in light of information currently available to us. Many important factors may adversely affect our results as indicated in forward-looking statements. These factors include, but are not limited to: our ability to attract prospective users and to retain existing users; our dependence upon third-party licenses for sound recordings and musical compositions; our lack of control over the providers of our content and their effect on our access to music and other content; our ability to generate sufficient revenue to be profitable or to generate positive cash flow on a sustained basis; our ability to comply with the many complex license agreements to which we are a party; our ability to accurately estimate the amounts payable under our license agreements; the limitations on our operating flexibility due to the minimum guarantees required under certain of our license agreements; our ability to obtain accurate and comprehensive information about music compositions in order to obtain necessary licenses or perform obligations under our existing license agreements; potential breaches of our security systems; assertions by third parties of infringement or other violations by us of their intellectual property rights; competition for users and user listening time; our ability to accurately estimate our user metrics and other estimates; risks associated with manipulation of stream counts and user accounts and unauthorized access to our services; changes in legislation or governmental regulations affecting us; ability to hire and retain key personnel; our ability to maintain, protect, and enhance our brand; risks associated with our international expansion, including difficulties obtaining rights to stream music on favorable terms; risks relating to the acquisition, investment, and disposition of companies or technologies; dilution resulting from additional share issuances; tax-related risks; the concentration of voting power among our founders who have and will continue to have substantial control over our business; risks related to our status as a foreign private issuer; international, national or local economic, social or political conditions; and risks associated with accounting estimates, currency fluctuations and foreign exchange controls.

Other sections of this report describe additional risk factors that could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time, and it is not possible for our management to predict all risk factors and uncertainties, nor are we able to assess the impact of all of these risk factors on our business or the extent to which any risk factor, or combination of risk factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements. You should read this report and the documents that we have filed as exhibits to this report completely and with the understanding that our actual future results may be materially different and worse from what we expect.

Interim condensed consolidated statement of operations

(Unaudited)

(in € millions, except share and per share data)

|

|

|

Three months ended |

|

|

Nine months ended |

|

||||||||||||||

|

|

|

September 30, |

|

|

June 30, |

|

|

September 30, |

|

|

September 30, |

|

|

September 30, |

|

|||||

|

Revenue |

|

|

1,731 |

|

|

|

1,667 |

|

|

|

1,352 |

|

|

|

4,909 |

|

|

|

3,764 |

|

|

Cost of revenue |

|

|

1,290 |

|

|

|

1,233 |

|

|

|

1,010 |

|

|

|

3,661 |

|

|

|

2,810 |

|

|

Gross profit |

|

|

441 |

|

|

|

434 |

|

|

|

342 |

|

|

|

1,248 |

|

|

|

954 |

|

|

Research and development |

|

|

136 |

|

|

|

151 |

|

|

|

135 |

|

|

|

442 |

|

|

|

393 |

|

|

Sales and marketing |

|

|

178 |

|

|

|

200 |

|

|

|

146 |

|

|

|

550 |

|

|

|

457 |

|

|

General and administrative |

|

|

73 |

|

|

|

86 |

|

|

|

67 |

|

|

|

252 |

|

|

|

241 |

|

|

|

|

|

387 |

|

|

|

437 |

|

|

|

348 |

|

|

|

1,244 |

|

|

|

1,091 |

|

|

Operating income/(loss) |

|

|

54 |

|

|

|

(3 |

) |

|

|

(6 |

) |

|

|

4 |

|

|

|

(137 |

) |

|

Finance income |

|

|

226 |

|

|

|

8 |

|

|

|

10 |

|

|

|

268 |

|

|

|

66 |

|

|

Finance costs |

|

|

(10 |

) |

|

|

(64 |

) |

|

|

(85 |

) |

|

|

(230 |

) |

|

|

(582 |

) |

|

Share in losses of associate |

|

|

— |

|

|

|

— |

|

|

|

(1 |

) |

|

|

— |

|

|

|

(1 |

) |

|

Finance income/(costs) – net |

|

|

216 |

|

|

|

(56 |

) |

|

|

(76 |

) |

|

|

38 |

|

|

|

(517 |

) |

|

Income/(loss) before tax |

|

|

270 |

|

|

|

(59 |

) |

|

|

(82 |

) |

|

|

42 |

|

|

|

(654 |

) |

|

Income tax expense/(benefit) |

|

|

29 |

|

|

|

17 |

|

|

|

(125 |

) |

|

|

19 |

|

|

|

(134 |

) |

|

Net income/(loss) attributable to owners of the parent |

|

|

241 |

|

|

|

(76 |

) |

|

|

43 |

|

|

|

23 |

|

|

|

(520 |

) |

|

Earnings/(loss) per share attributable to owners of the parent |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

1.34 |

|

|

|

(0.42 |

) |

|

|

0.24 |

|

|

|

0.13 |

|

|

|

(2.96 |

) |

|

Diluted |

|

|

0.36 |

|

|

|

(0.42 |

) |

|

|

0.23 |

|

|

|

0.09 |

|

|

|

(2.96 |

) |

|

Weighted-average ordinary shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

179,863,596 |

|

|

|

180,409,115 |

|

|

|

180,510,524 |

|

|

|

180,292,670 |

|

|

|

175,835,503 |

|

|

Diluted |

|

|

188,477,554 |

|

|

|

180,409,115 |

|

|

|

188,120,122 |

|

|

|

185,788,598 |

|

|

|

175,835,503 |

|

Condensed consolidated statement of financial position

(Unaudited)

(in € millions)

|

|

|

September 30, |

|

|

December 31, |

|

||

|

Assets |

|

|

|

|

|

|

|

|

|

Non-current assets |

|

|

|

|

|

|

|

|

|

Lease right-of-use assets |

|

|

486 |

|

|

|

— |

|

|

Property and equipment |

|

|

270 |

|

|

|

197 |

|

|

Goodwill |

|

|

489 |

|

|

|

146 |

|

|

Intangible assets |

|

|

58 |

|

|

|

28 |

|

|

Long term investments |

|

|

1,678 |

|

|

|

1,646 |

|

|

Restricted cash and other non-current assets |

|

|

68 |

|

|

|

65 |

|

|

Deferred tax assets |

|

|

9 |

|

|

|

8 |

|

|

|

|

|

3,058 |

|

|

|

2,090 |

|

|

Current assets |

|

|

|

|

|

|

|

|

|

Trade and other receivables |

|

|

386 |

|

|

|

400 |

|

|

Income tax receivable |

|

|

2 |

|

|

|

2 |

|

|

Short term investments |

|

|

640 |

|

|

|

915 |

|

|

Cash and cash equivalents |

|

|

877 |

|

|

|

891 |

|

|

Other current assets |

|

|

73 |

|

|

|

38 |

|

|

|

|

|

1,978 |

|

|

|

2,246 |

|

|

Total assets |

|

|

5,036 |

|

|

|

4,336 |

|

|

Equity and liabilities |

|

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

|

|

|

Share capital |

|

|

— |

|

|

|

— |

|

|

Other paid in capital |

|

|

3,884 |

|

|

|

3,801 |

|

|

Treasury shares |

|

|

(494 |

) |

|

|

(77 |

) |

|

Other reserves |

|

|

1,052 |

|

|

|

875 |

|

|

Accumulated deficit |

|

|

(2,500 |

) |

|

|

(2,505 |

) |

|

Equity attributable to owners of the parent |

|

|

1,942 |

|

|

|

2,094 |

|

|

Non-current liabilities |

|

|

|

|

|

|

|

|

|

Lease liabilities |

|

|

618 |

|

|

|

— |

|

|

Accrued expenses and other liabilities |

|

|

13 |

|

|

|

85 |

|

|

Provisions |

|

|

6 |

|

|

|

8 |

|

|

Deferred tax liabilities |

|

|

1 |

|

|

|

2 |

|

|

|

|

|

638 |

|

|

|

95 |

|

|

Current liabilities |

|

|

|

|

|

|

|

|

|

Trade and other payables |

|

|

519 |

|

|

|

427 |

|

|

Income tax payable |

|

|

8 |

|

|

|

5 |

|

|

Deferred revenue |

|

|

308 |

|

|

|

258 |

|

|

Accrued expenses and other liabilities |

|

|

1,259 |

|

|

|

1,076 |

|

|

Provisions |

|

|

8 |

|

|

|

42 |

|

|

Derivative liabilities |

|

|

354 |

|

|

|

339 |

|

|

|

|

|

2,456 |

|

|

|

2,147 |

|

|

Total liabilities |

|

|

3,094 |

|

|

|

2,242 |

|

|

Total equity and liabilities |

|

|

5,036 |

|

|

|

4,336 |

|

Contacts

Investor Relations:

Paul Vogel

ir@spotify.com

Public Relations:

Dustee Jenkins

press@spotify.com